Answer:

a. hunters

Explanation:

Hunters are also known as who deal with doing. Sales energy is gained by "hunting for new opportunities". Hunters can be designated as independent (multiple initiative) and solution-oriented. As they close their existing opportunities, they tend to make big deals by excelling as:

- Account Manager

- Area sales representative

- Business Development Representative / Manager

Answer:

The correct answer is (D)

Explanation:

Sometimes firms and organisations try to reduce the outstanding stocks in the market. To do so, they purchase back some of those stocks from the open market, such stocks are known as treasury stocks. After that, It is up to the issuer, they can resell it to the public or they can dissolve them completely. After purchasing back, these stocks are no longer considered outstanding.

Some solutions when your child cannot go to sleep would be:

Your baby needs to learn how to comfort himself and put himself back to sleep. You can begin slowly by introducing a soft toy or blankie during cuddle time.

It's important to teach your blind baby the cues that indicate a shift from day to night. This means that you will want to establish a pretty strict night time routine

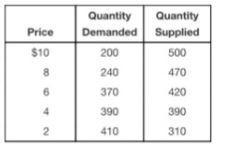

If there was a 100 units decrease at every price level, the new equilibrium price would be<u> $2.00.</u>

<h3>Equilibrium Price </h3>

- Price where quantity demanded is equal to quantity supplied.

<h3>What is the New Equilibrium price?</h3>

Reducing by 100 units, all the quantity demanded units will lead to the following new units:

- $10 - 100

- $8 - 140

- $6 - 270

- $4 - 290

- $2 - 310

We can see that at $2, both the demand and supply are at 310 units which makes this the new equilibrium.

Find out more on the equilibrium price at brainly.com/question/14203212.

Answer: Option c

Explanation: In simple words, the capital asset pricing model (CAPM) is a model used to determine an asset's hypothetically suitable necessary return rate to decide to attach assets to a diversified portfolio.

The equation takes into consideration the exposure of the asset to non-verifiable uncertainty , also expressed by the quantity beta (β) in the financial industry, as well as the expected market return and the expected return of a risk-free hypothetical asset.

Hence from the above we can conclude that the correct option is .