Answer: Constructive criticism encourages growth and learning by being positive and encouraging, offering solutions to problems, targeting specific areas for improvement and by being expressed only in private.

Explanation:

Here is the correct question:

Support this statement using complete sentences: “Constructive criticism is offered in a way that encourages growth and learning.”

Constructive criticism is when an individual offers valid opinions about what others have done in a way that doesn't fault the person but rather encourages the person to improve.

The person offered constructive criticism should not be criticised in public but rather praised in public while he or she is then criticised in private. Criticism should be done in a friendly manner and not an unfriendly or aggressive manner.

Answer:

14.81%

Explanation:

Unemployment rate = (unemployed people/ labour force ) x 100

Labour force = unemployed people + employed people

= 230 million + 40 million = 270 million

(40 / 270) × 100 = 14.81%

I hope my answer helps you

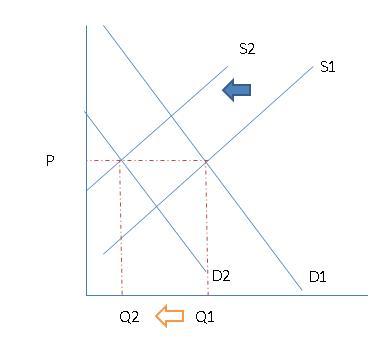

Answer:

The equilibrium quantities of lettuce reduces and price remains the same.

Explanation:

In the attached image is the grapichal analysis of the reduction of demand and supply in the same proportion.

The two major causes of postoperative wound evisceration are as follows,

- Post-surgery wound stress, which might involve something as simple as a cough or sneeze

- Certain sutures may disintegrate too quickly, causing the wound to open.

- The type of closure employed, may or may not have been beneficial for the incision.

What is evisceration?

Evisceration is a rare but serious surgical complication in which the surgical incision opens and the abdominal organs protrude or come out. Evisceration is a medical emergency that must be treated as such.

- It can range from mild to severe, with the organs exposed and slightly protruding outside of the incision.

- Intestines, for example, may leak from an abdominal incision.

- This is usually considered a medical emergency.

- If you notice tissue or organs emerging from a surgical site, call your doctor.

- It is critical to keep the wound wet. Cover the opening and organs with a wet, sterile bandage or sheet while on your route to seek medical help or while waiting for EMS.

Learn more about Evisceration here,

brainly.com/question/4224130

# SPJ4