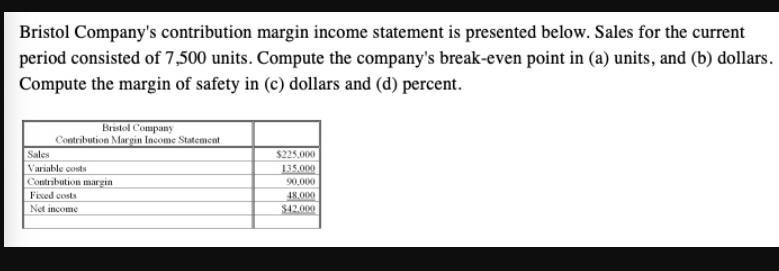

Answer and Explanation:

The computation is shown below:

The Selling price per unit = $225,000 ÷ 7500 = $30

ANd,

Variable cost per unit = $135,000 ÷ 7500 = $18

a) Breakeven point = Fixed cost ÷ Contribution margin per unit

= $48,000 ÷ ($30 - $18)

= 4000 units

b) Breakeven dollars = Breakeven point × selling price per unit

= 4000 × 30

= $120,000

C) Margin of Safety in dollars = Sales Revenue - Breakeven dollars

= $225,000 - $120,000

= $105,000

d) Margin of Safety in percent

= $105,000 ÷ $225,000

= 46.67%

<span>the type of risk that is most likely to be insurable is : A. pure risk

Pure risk refer to the type of risk in which loss is the only possible outcome.

Example of pure risk : Identitiy theft

Identity theft is insurable because the only possible outcome of identity theft is a loss in assets, there is no way someone could get more wealth after identity theft</span>

Jack is making an assumption while john is making a believable excuse

Answer:

This means that receiving 9000 today is better for us as we will have more at the end of 6 years.

Explanation:

We need to first calculate what is the future value of payments in both scenarios. If we receive $9,000 today and invest it at 10% for 6 years we will have 9000*1.10^6=15,944

If we start reviving cash in 4 annual payments 2 years from now of $3000 we will have to find the future value of each individual payment and add them up.

First payment Future value = 3000*1.10^4=4392 (Money can be invested for 4 years at 10%)

Second payment future value = 3000*1.10^3=3993 (Money can be invested for 3 years at 10%)

Third payment future value = 3000*1.10^2=3630 (Money can be invested for 4 years at 10%)

Fourth payment future value = 3000*1.1=3300

Add them all up = 15315

This means that receiving 9000 today is better for us as we will have more at the end of 6 years.

Answer:

Correct answer is (e). Is a court order prohibiting certain activities in conjunction with a labor dispute.

Explanation:

An injunction is an instrument used in mitigating against some industrial action such as strikes and boycotts. It's a court order used to instruct party to do, or refrain from doing a particular act.