Answer:

Bond Price = $875.6574005 rounded off to $875.66

Explanation:

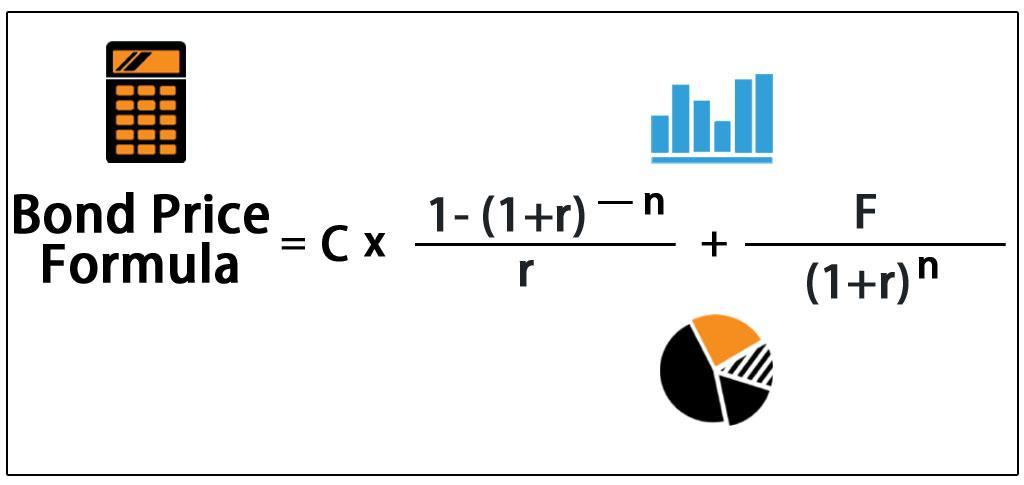

To calculate the price of the bond today, we will use the formula for the price of the bond. We assume that the interest rate provided is stated in annual terms. As the bond is an annual bond, the coupon payment, number of periods and annual YTM will be,

Coupon Payment (C) = 1,000 * 0.05 = $50

Total periods (n) = 3

r or YTM = 0.10

The formula to calculate the price of the bonds today is attached.

Bond Price = 50 * [( 1 - (1+0.10)^-3) / 0.10] + 1000 / (1+0.10)^3

Bond Price = $875.6574005 rounded off to $875.66

Answer:

Option B.

Explanation:

Basic accounting equation is

Assets = Liabilities + Equity

where,

Equity = Capital + Retained earnings

Retained earnings = Revenue - Expenses - Dividend

On combining these formula, we get

Assets = Liabilities + Capital + Revenue - Expenses - Dividend

It can be rewritten as

Assets + Dividend + Expenses = Liabilities + Capital + Revenue

Assets + Dividends + Expenses = Liabilities + Common stock + Retained Earnings + Revenues

Therefore, the correct option is B.

Answer: b. Because the opportunity cost of the fourth unit of capital is the consumption goods that must be given up for this economy to move from three units of capital to four units of capital, but the opportunity cost of four units of capital is the amount of consumption goods that must be given up to go from zero units of capital to four units of capital.

Explanation:

The opportunity cost of the 4th unit of capital refers to how many units of consumption need to be given up for the economy to move from the third unit to the forth unit of capital. In other words, the economy needs to give up 4 more goods to move from the 3rd unit of capital to the fourth.

But if the Economy was to produce the entire 4 units of capital it would have to give up the entire 10 units of consumption in total.

Answer:

b. coercion

Explanation:

A manager who threatens to withhold support or rewards is using coercion as a political tactic. Employees who work under a coercive management, are forced to follow orders and face a harsh and negative work environment that often leads employees to look for other jobs. Managers who practice coercion feel powerful and might but they don't realize how much damage it causes in the long run for the organization.