Answer:(a) Sales 81,000,000 (b ) sales in unit 6,000,000 (c) Cost of good sold Variable 21,645,000 fixed 24,033,769.16 (d) 35,321,230.84 (e ) Attributable Cost, Marketing cost 5,580,000, Other (primarily fixed ) 2,580,475.425 (g) Product line profit beforeG&A Allocation 27,160,755.42 (h) Return on Sales 33.5%, The product manager would meet his profit target of 25% on Sales in 2007

Explanation:

The question is not complete, here is the missing part of the question

First class ovenware income statements for the year ended 31st December 2002-2006

2006. 2005. 2004. 2003

Sales. 78,599,808. 81,874,800. 86,184,000. 75,600,000

Sales in unit 5,239,987. 5,458,320. 5,745,600. 5,040,000

Cost of Good Sold

Variable. 29,081,929. 31,112,424. 31,026,240. 27,972,000

Fixed. 27,865,240. 23,221,033. 21,701,900. 19,729,000

Gross Profit. 21,652,639. 27,541,343. 33,455,860. 27,899,000

Attributable Cost

Marketing cost. 5,894,986. 6,140,610. 5,774,328. 5,140,800

Other(primarily fixed ) 2,517,537. 2,502,522. 2,317,150. 2,106,500

Product line profit

Before G&A Allocation. 13,240,117. 18,898,211. 25,364,382. 20,651,700

Return on Sales. 16.84% 23.08% 29.43% 27.32%

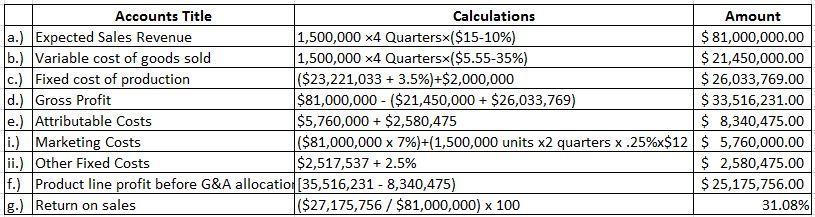

Here is the solution

First class ovenware budgeted income statement for the year ended December 31st 2007

Sales. 81,000,000

Sales unit. 6,000,000

Cost of Good Sold

Variable 21,645,000

Fixed 24,033,769.16

Gross Profit. 35,321,230.84

Attributable Cost

Marketing cost. 5,580,000

Other(primarily fixed ) 2,580,475.425

Product line profit before G&A Allocation 27,160,755.42

Return on Sales 33.5%

Workings

Sales 6,000,000 × $15 = 90,000,000

10% × 90,000,000 = 9,000,000

Sales in unit 1,500,000 × 4 = 6,000,000

Cost of Good Sold

Variable ($5.55 - 35%) × 6,000,000

= 35% × 5.55 = 1.9425

= 5.55 - 1.9425 = 3.6075 × 6,000,000 = 21,645,000

Fixed ( fixed cost 2005 + 3.5%)

( 23,221,033 + 3.5%)

= 3.5% × 23,221,033 = 812,736.155

= 23,221,033 + 812,736.155 = 24,033,769.16

Gross Profit = Sales - Variable cost + Fixed cost

Variable cost + Fixed cost

= 21,645,000 + 24,033,769.16

=45,678,769.16

81,000,000 - 45,678,769.16

= 35,321,230.84

Attributable Cost

Marketing cost = 6,000,000 × 7% = 420,000

6,000,000 - 420,000 = 5,580,000

Other ( primarily fixed) Fixed cost 2006 ( 1 + 2.5%)

= 2,517,537 ( 1 + 0.025)

= 2,517,537 ( 1.025)

= 2,580,475.425

Product line profit before G & A Allocation = Gross Profit - Attributable Cost

= 35, 321,230.84 - 8,160,475. 425

= 27,160,755.42

Return on Sales = Product line profit before G&A Allocation / Sales

= 27,160,755.42 / 81,000,000

= 0.335

= 0.335 × 100

= 33.5%