Answer:

A) company HD pays less in Tax

Explanation:

Because interest is deducted before tax in income statement. Higher interest means less Earning before tax, and less amount of Tax be deducted.

HD and LD both have same Earning before interest and tax.

Let suppose both have EBIT of $1000,

Not HD has interest expense of 150, and LD has interest expense of $100

Now HD Earning before tax would be 850, and LD EBT would be 900.

Let's say tax is 40%

so,

HD tax would be 850*0.4=340

LD tax would be 900*0.4=360

So, HD pays higher interest, it benefit company in paying lower tax amount. bacause interest is tax saving.

HD saves $20 in this hypothetical example.

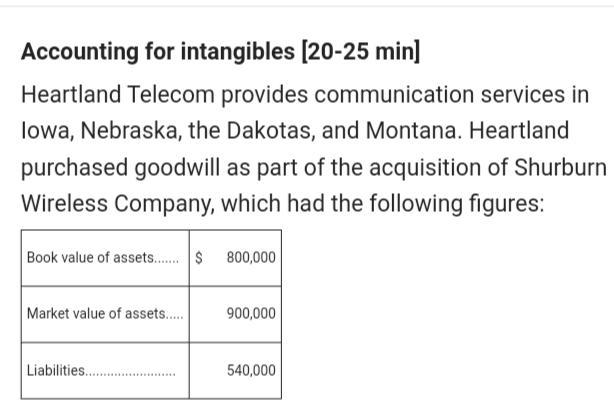

Answer: 1. Goodwill

2. a. Record no entry in the books

b. Record a loss in the books

Explanation:

1. The Special asset created by Heartland Telecom's acquisition of Surety Wireless is Goodwill.

Goodwill is the difference between what the company was worth and what it was purchased for if the purchase price was higher than the worth (market value).

2. a. Goodwill should be accounted for by recoding it in the Long term Assets under Intangible Assets in the balance sheet. It should not be amotrized. If Goodwill increases, there should be no recording this <u>gain</u> on the books.

b. If the value of the asset has decreased, Heartland should record a loss in the books to represent the loss on this account.

Answer:

A, B, and D are the answers

Explanation:

Answer:

The best answer to the question: This is an example of used a(n):___, would be, A: Conceptual framework to solve new problems.

Explanation:

A conceptual framework is a an analytical method, or technique, that is used in order for the person to be able to see the full picture, and the different variants and factors around it, in an organized manner. Applying this technique will allow a person to discover all the factor within an issue, visualize them and propose viable solutions to them. And this is what Mark did when he came by the non-standard transaction type. He still had to record the transaction, but the usual methods would not work for it. Therefore, Mark made use of his own knowledge and after viewing the problem through the conceptual framework technique, he was able to find a reasonable solution and thus filfill his job.