Answer:

In the real world, pollution is served as an example of market failure. ... According to the diagram, in this case pollution, negative externalities occurs. At the output Qe , equilibrium output is achieved by the firm, at which the marginal private cost equals the price of the firm's output.

That would be B.) Programming code for a video game, since Intellectual property<span> (IP) refers to creations of the mind, such as inventions; literary and artistic works; designs; and symbols, names and images used in commerce.

I hope this answer helped you! If you have any further questions or concerns, feel free to ask! :)

</span>

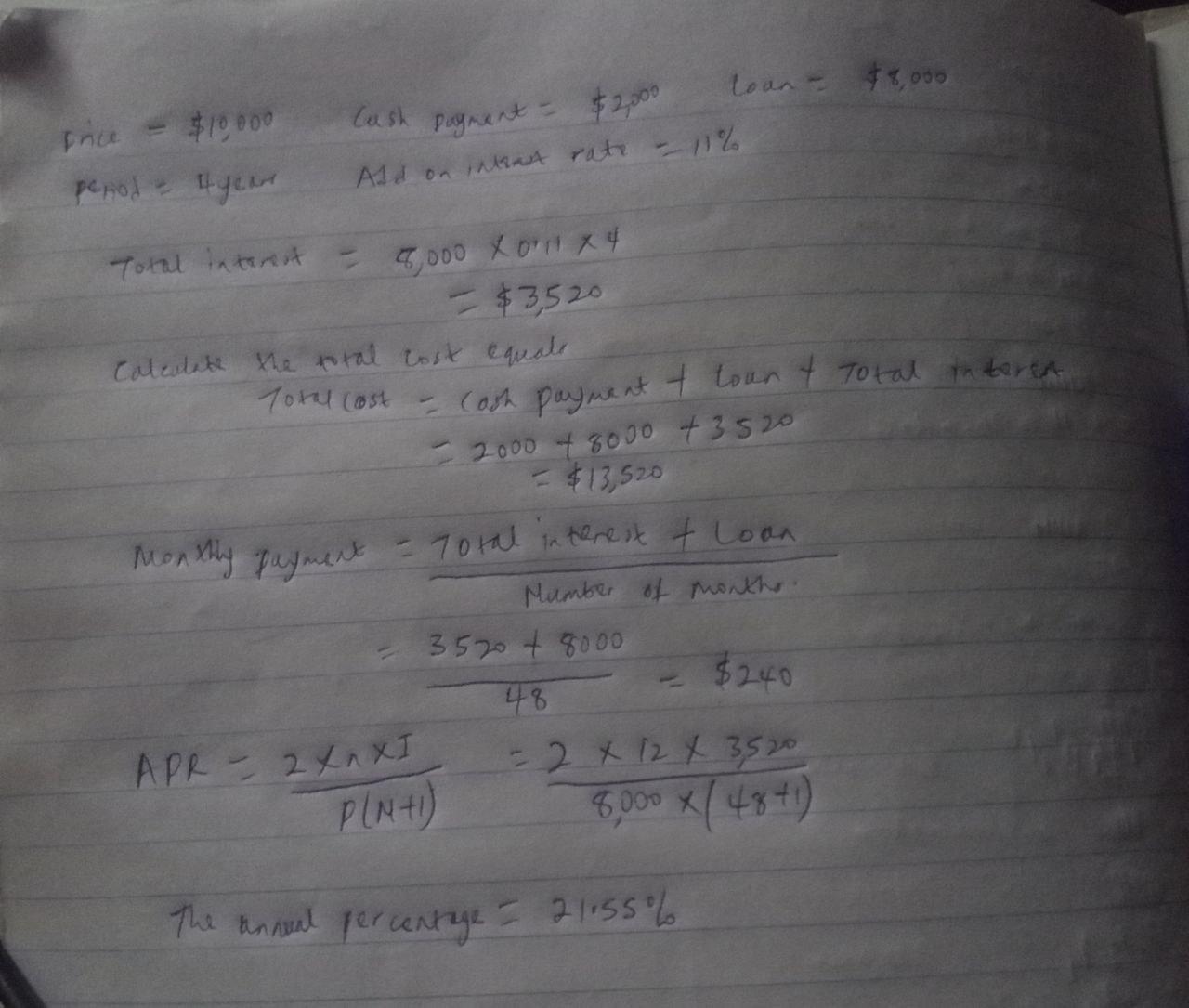

Answer:

Explanation:

The picture attached shows the explanation

Trader joes differentiate itself from competitors by offering top-quality foods obtained through sustainable agriculture. This business strategy implies that trader joes focus on gaining a market share and making up the loss in margin through increased sales.

According to the Cost Leadership article, Trader Joe's focuses on low-cost, high-quality products to attract customers' attention. Trader Joe's is a very small store less than 10,000 square feet.

Just Right Airline is probably sitting in the middle because it's basically trying to reconcile different strategic positions (high-quality features versus low price). Other airlines consistently pursue either differentiation or low-cost strategies.

Marriott has reduced its cost structure by distributing its manufacturing facilities across multiple hotel types, increasing the diversity and differentiated appeal of its hotel line.

Learn more about Trader joes at

brainly.com/question/24130059

#SPJ4