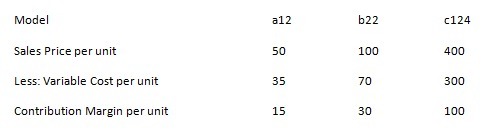

The first step you need to do to solve this problem is to

calculate the contribution margin per unit for each model:

Model a12 b22 c124

Sales Price per unit 50 100 400

Less: Variable Cost per unit 35 70 300

Contribution Margin per unit 15 30 100

The next step is to calculate the weighted-average

contribution margin per unit for the sales mix using the following formula:

Model a12 CM per Unit ×

Model a12 Sales Mix Percentage<span>

+ Model b22 CM per Unit × Model b22 Sales Mix Percentage

+ Model c124 CM per Unit × Model c124 Sales Mix Percentage

<span>= Weighted Average Unit Contribution Margin (WACM)</span></span>

Contribution Margin per unit 15 30 100

X Sales Mix Percentage 60% 15% 25%

WACM 9 4.5 25

Weighted Average Unit Contribution Margin (sum) 38.5

The next step is to find the break-even point using the

WACM.

<span>

<span><span>

<span>

Total Fixed Cost

</span>

<span>

$269,500

</span>

</span>

<span>

<span>

÷ Weighted Average CM per Unit

</span>

<span>

$38.50

</span>

</span>

<span>

<span>

Break-even Point in Units of Sales Mix

</span>

<span>

7,000

</span>

</span>

</span></span>

The next step is to calculate the number of units of each

model at break-even point

<span>

<span><span>

<span>

Model

</span>

<span>

a12

</span>

<span>

b22

</span>

<span>

c124

</span>

</span>

<span>

<span>

Sales Mix Ratio

</span>

<span>

60%

</span>

<span>

15%

</span>

<span>

25%

</span>

</span>

<span>

<span>

× Total Break-even Units

</span>

<span>

7,000

</span>

<span>

7,000

</span>

<span>

7,000

</span>

</span>

<span>

<span>

Product Units at Break-even Point

</span>

<span>

4,200

</span>

<span>

1,050

</span>

<span>

1,750

</span>

</span>

</span></span>

<span> </span>