Answer:

a-1) Pv = 52549

a-2) Pv = 56822

b-1) Fv = 77570

b-2 Fv = 83878

Explanation:

b-1) Future value:

S= Sum of amount of annuity=?

n=number of fixed periods=5 years

R=Fixed regular payments=13200

i=Compound interest rate= .081 (suppose annualy)

we know that ordinary annuity:

S= R [(1+i)∧n-1)]/i

= 13200[(1+.081)∧5-1]/.081

=13200(1.476-1)/.081

= 13200 * 5.8765

S = 77570

a.1)Present value of ordinary annuity:

Formula: Present value = C* [(1-(1+i)∧-n)]/i

=13200 * [(1-(1+.081)∧-5]/.081

=13200 * (1-.6774)/.081

=13200 * (.3225/.081)

=52549

a.2)Present value of ordinary Due:

Formula : Present value = C * [(1-(1+i)∧-n)]/i * (1+i)

= 13200 * [(1- (1+.081)∧-5)/.081 * (1+.081)

= 13200 * 3.9822 * 1.081

= 56822

b-2) Future value=?

we know that: S= R [(1+i)∧n+1)-1]/i ] -R

= 13200[ [ (1+.081)∧ 5+1 ]-1/.081] - 13200

= 13200 (.5957/.081) -13200

= (13200 * 7.3544)-13200

= 97078 - 13200

= 83878

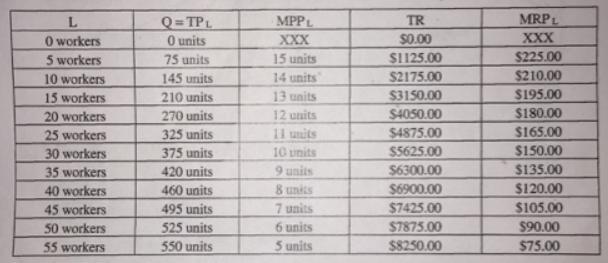

Answer: B. The firm hires 45 workers and earns a $1,200.00 Economic Profit

Explanation:

If the Market Equilibrium rate is $105 then the company should hire 45 workers as shown in the table.

If they did that, revenue would be $7,425

Expenses would be wages and fixed costs:

= Wages + fixed costs

= (45 workers * wage rate) + 1,500

= (45 * 105) + 1,500

= $6,225

Economic profit would be:

= 7,425 - 6,225

= $1,200

Answer:

Childress Company

Orders for K1 should be filled first.

Orders for G9 should be filled second.

Orders for S5 should be filled third.

Explanation:

a) Data and Calculations:

K1 S5 G9

Direct materials per unit (pounds) 4.9 2.4 5.4

Materials available for production = 58,400

Selling price $ 167.40 $ 99.28 $ 210.02

Variable costs 89.00 76.00 149.00

Contribution margin per unit $ 78.40 $ 23.28 $ 61.02

Contribution margin per pound $16 $9.70 $11.30

Orders for K1 should be filled first

Orders for G9 should be filled second

Orders for S5 should be filled third.

b) This order filling sequence will maximize the contribution margin per pound, ensuring the highest efficient use of the limited materials available for production.

Answer:

The answer is letter A.

Explanation:

Determining salesperson targets and incentives is a preproduction service in a value chain that requires forecasts to gain customers in the value chain.

Answer:

D. period costs.

Explanation:

The period cost is the cost which is incurred during the passage of time. It includes the major part of the ling and administrative expenses of the income statement. This cost is not capitalized. It is to be allocated based on the expenses that are against the revenue.

Example - Depreciation on delivery trucks, advertising expense, etc