<h3>

Answer:</h3>

Debiting salaries Expense $400 and Crediting Salaries payable $400.

<h3>

Explanation:</h3>

We are given;

1 employees earns $ 100 a day

Therefore;

2 employees will earn $ 200 a day

The month ends on Tuesday, but the two employees works on Monday and Tuesday.

- Therefore, the month-end adjusting entry to record will be the amount earned by the two employees on the two days.

Two employees for 2 days = $200/day × 2 days

= $400

- But, salary is an expense, and in the accounts an increase in expense account is debited.

- According to the rule of double entry, an increase in salaries expense decreases the salaries payable. Therefore, we debit salaries expense account and credit salaries payable account.

- Therefore, the month-end adjusting entry to record the salaries earned but unpaid would be;

Debiting salaries Expense $400 and Crediting Salaries payable $400.

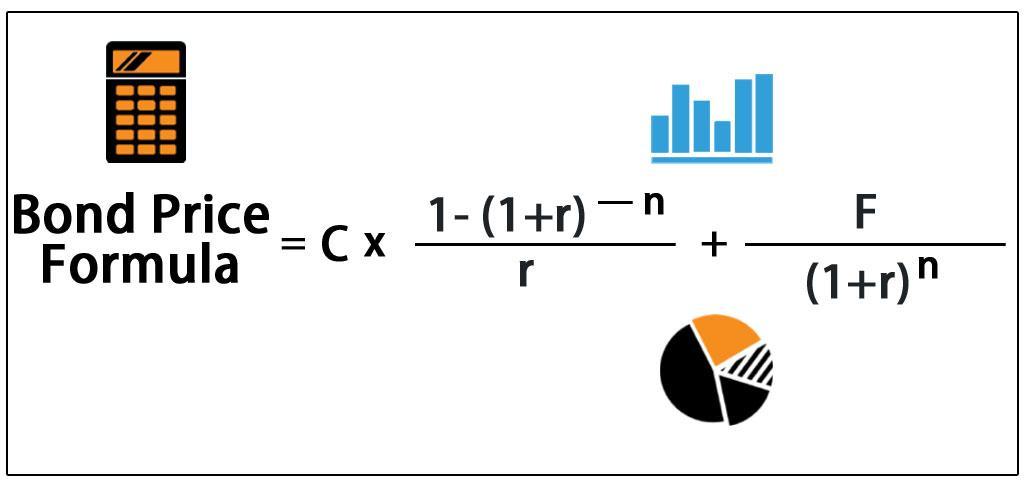

Answer:

Bond Price = $951.9633746 rounded off to $951.96

Explanation:

To calculate the quote/price of the bond today, which is the present value of the bond, we will use the formula for the price of the bond. As the bond is an annual bond, we will use the annual coupon payment, annual number of periods and annual YTM. The formula to calculate the price of the bonds today is attached.

Coupon Payment (C) = 1000 * 10% = $100

Total periods remaining (n) = 3

r or YTM = 12%

Bond Price = 100 * [( 1 - (1+0.12)^-3) / 0.12] + 1000 / (1+0.12)^3

Bond Price = $951.9633746 rounded off to $951.96

Answer: d. A provision related to the achievement of certain performance criteria

Explanation:

While compensatory plans are used in order to compensate the employees of a particular company, the noncompensatory stock option is one whereby the employees of a company are allowed to purchase the stock of that company at a particular price t a specific price and at a particular time period.

Some of its characteristics include:

• participation by substantially all full-time employees who meet limited employment qualifications.

• equal offers of stock to all eligible employees.

• a limited amount of time permitted to exercise the option.

Option D that "provision related to the achievement of certain performance criteria" isn't a characteristics. Therefore, D is the answer.

Answer: The GDP deflator

Explanation: The GDP(gross domestic product) deflator is a price index that is used to measure the prices of all the goods and services produced within an economy. The cars which are exported by General Motors are produced domestically within the United States of America and exported outside the country.

Any goods produced externally are not considered when determining the GDP deflator.

Answer:

Reserve. resource

Explanation:

concentration of natural minerals in or on the crust of the Earth with potential to be extracted for profit.