Answer:

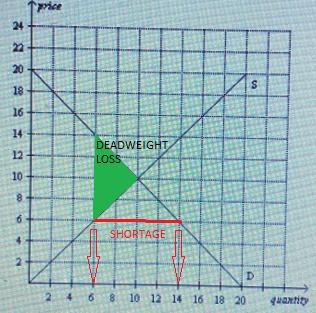

A price ceiling set at $6 will be binding and will result in a shortage of 8 units.

Explanation:

In order for a price ceiling to be binding, it must be set below the equilibrium price level. In this case, $6 is below the equilibrium price of $10. It will produce a shortage of 8 units because the quantity supplied by producers will be only 6 units, while the quantity demanded by consumers will be 14 units.

Binding price ceilings always produce a deadweight loss which is represented by the area between the demand curve and the supply curve left to the equilibrium price.

The interest would be 11.61232% to be exact.

Answer: Yes, the rights of the child can help them in their development.

Explanation: Organizations such as UNICEF explain that children have a series of rights that are essential for them to have a healthy development and to become good adults. Children have the right to a family structure and to be cared for, since when they are young there are many things that they cannot do for themselves and they need others to achieve it. An example of this would be that children must be sent to school by their parents. Children have the right to an education.

Answer and Explanation:

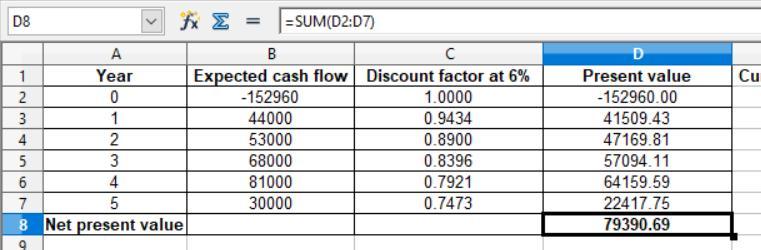

The computation of the net present value is presented in the attachment below:

For project A, the net present value is $91,771.53 and for project B, the net present value is $79,390.69

It is computed after considering the discounting factor that comes from

= 1 ÷ (1 + discount rate)^number of years

for year 1, it is

= 1 ÷ (1 + 0.06)^1

The same applied for the remaining years