Answer:

= 18 cm^3

Step-by-step explanation:

V = Bh where B is the area of the base, which is the triangular face

B = 1/2 (4*3) = 6

V = 6* 3

V = 18 cm^3

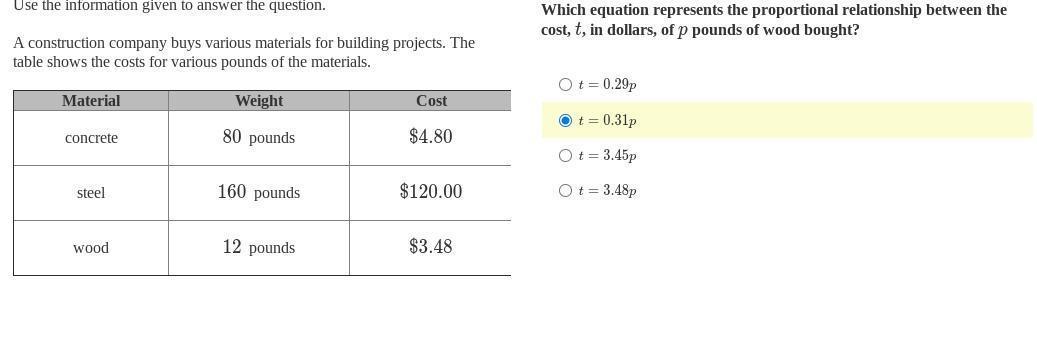

Answer:

T = 0.29p

Step-by-step explanation:

From the table Given :

We can obtain the uint cost per pound of wood :

Cost of 12 pounds of wood = $3.48

Cost per pound = Cost / weight

Cost per pound = $3.48 / 12 = $0.29

Hence, the proportional relationship cost, T in dollars and p pounds of wood is ;

Cost = unit cost per pound * number of pounds

T = 0.29 * p

T = 0.29p

Answer:

C.

Step-by-step explanation:

The highest term must be of x^4, then decreasing to x^3, x^2, x and the constant term.

Altogether there are at maximum 5 terms.

Answer:

(x - 3)(x - 12)

x would = 3 and 12

Step-by-step explanation: