Answer:

Explanation:

1. Number of goods available for sale = Beginning Inventory + Purchase, March 5 + Purchase, September 19 = 4,000+10,000+6,000 = 20,000 units

Cost of goods available for sale = Beginning Cost of inventory + Cost of Purchase, March 5 + Cost of Purchase, September 19 = 4,000×24 + 10,000×25 + 6,000×27 = 96,000+250,000+162,000 = $508,000

2. Number of units in ending inventory = Number of units available for sale - Number of units sold = 20,000-4,200-9,000 = 6,800 units

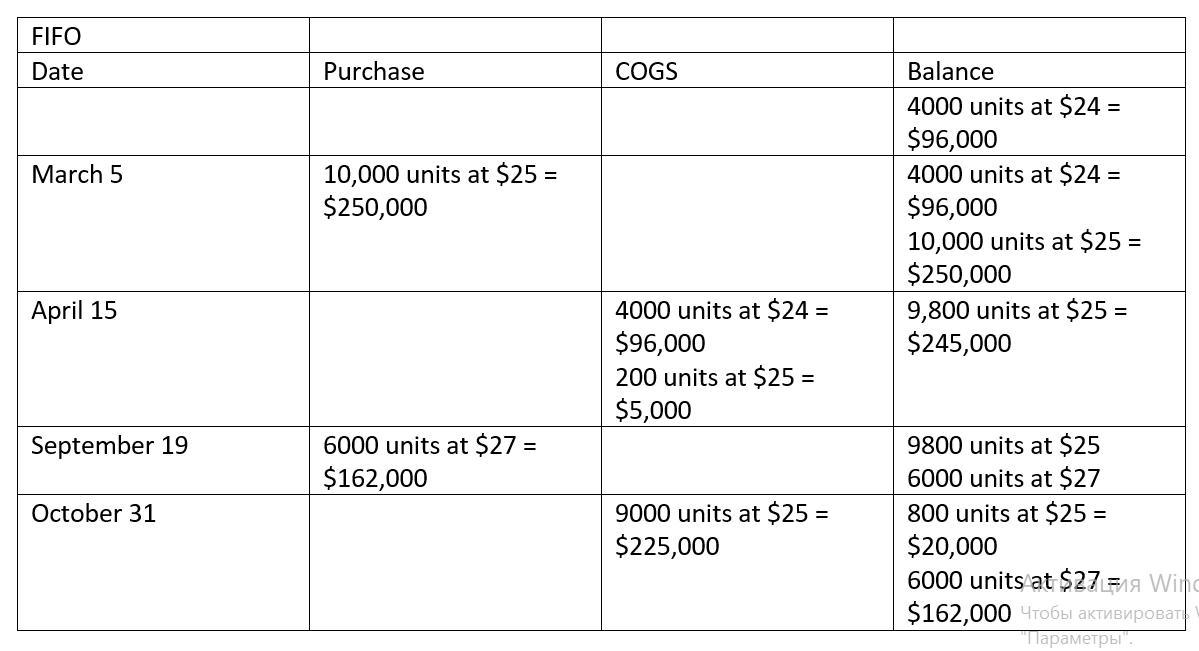

3. Calculations are attached

4.

Income statement FIFO:

Sales $937,800 (4,200×69 + 9,000×72)

Less: Cost of Goods Sold ($326,000)

Gross profit $611,800

Less Operating expense $602,000

Net income $9,800

Income statement LIFO:

Sales $937,800 (4,200×69 + 9,000×72)

Less: Cost of Goods Sold ($342,000)

Gross profit $595,800

Less Operating expense $602,000

Net loss $($6,200)

Income statement LIFO:

Sales $937,800 (4,200×69 + 9,000×72)

Less: Cost of Goods Sold ($334,092)

Gross profit $603,708

Less Operating expense $602,000

Net income $1,708

**Cost of goods sold:-

Under FIFO = 96,000+5,000+225,000 = $326,000

Under LIFO = 105,000+162,000+75,000 = $342,000

Under weighted average method = 103,782+230,310 = $334,092

6. LIFO method minimize taxes