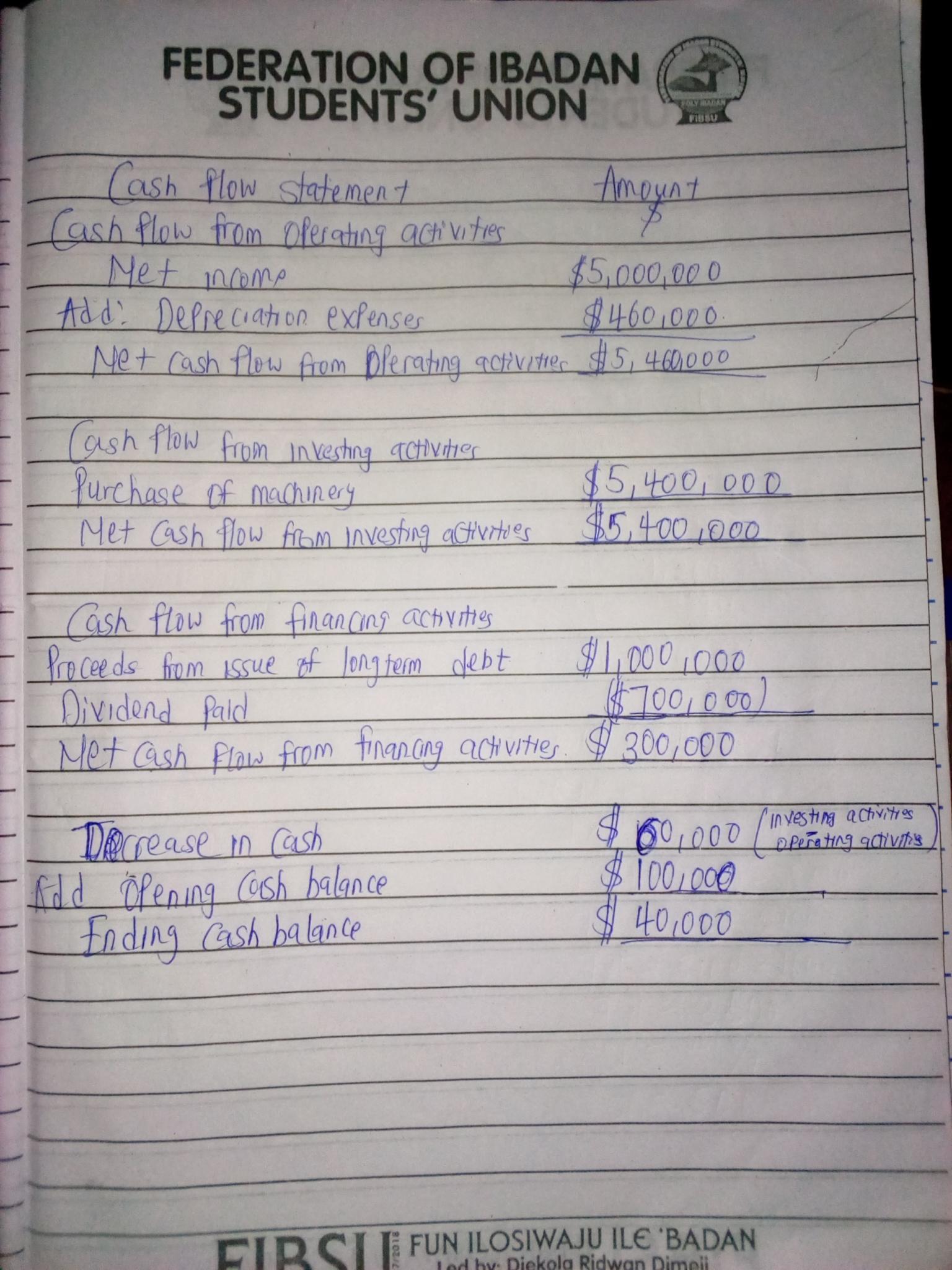

Answer:

The ending cash balance is $40,000

Explanation:

Kindly check attached picture for detailed explanation on Cash Flow statement

The answer is increas taxes think bout it' if u decrease it would make it worse

Answer:

. C) a drop in the foreign exchange value of the dollar.

Explanation:

An aggregate demand curve can be regarded as a curve that display total spending that is available

domestic goods/services with respect to their price level. the horizontal axis provide the real GDP while price level is displayed by vertical axis. It should be noted that The aggregate demand curve would shift to the right as a result a drop in the foreign exchange value of the dollar.

What is inflation?

Monetary value of final goods and services produced within a country for a specific time period.