Answer and Explanation:

1. The discount rate is

If we go through the options

like we assume 10%

So, the net present value is

= ($250,000 × 4.3553) - $1,000,000

= $1,088,825 - $1,000,000

= $88,825

Now if the discount rate is 11%

So, the net present value os

= ($250,000 × 4.2305) - $1,000,000

= $1,057,625 - $1,000,000

= $57,625

So the net present value is $57,625

2. The profitability index is

= ($1,000,000 + $57,625) ÷ ($1,000,000)

= 1.058

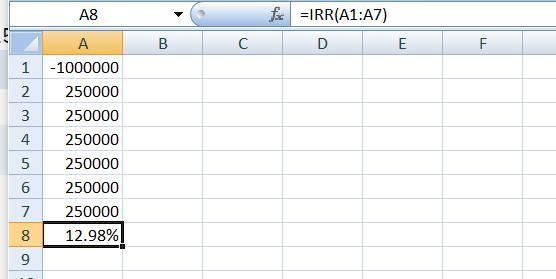

3. The internal rate of return is

It is 12.98% that lies between 12.5% and 13%