Answer:

$(123,000) + $(29,000)= $(152,000)

Explanation:

Discontinued operations are those operations of segment of a company where a formal plan exists to eliminate it from the company.

The revenues, gains, expenses, and losses pertaining to the discounting business segment are removed from the company's continuing operations and are reported separately on the company's income statement.

Hence, operating loss of $ 123,000 and impairment loss of $ 29,000 will separately be reported on income statement of the company.

Future estimated operating losses do not become part of the income statement.

Answer:

The firm's unleveraged beta is 1.0251

Explanation:

Hamada's equation is used to separate the financial risk of a levered firm from its business risk.

The Hamada equation:

Bu= Bl/(1 + (1 − T)(D/E))

Bl = 1.4

wd = 0.36

Tax rate = 35%

D/E = wd / (1 – wd) = 0.5625 = 56.25%

= 1.4/ (1+(1-0.35)(0.5625))

=1.4/ 1 + (0.65)(0.5625)

=1.4/1.36

= 1.0251

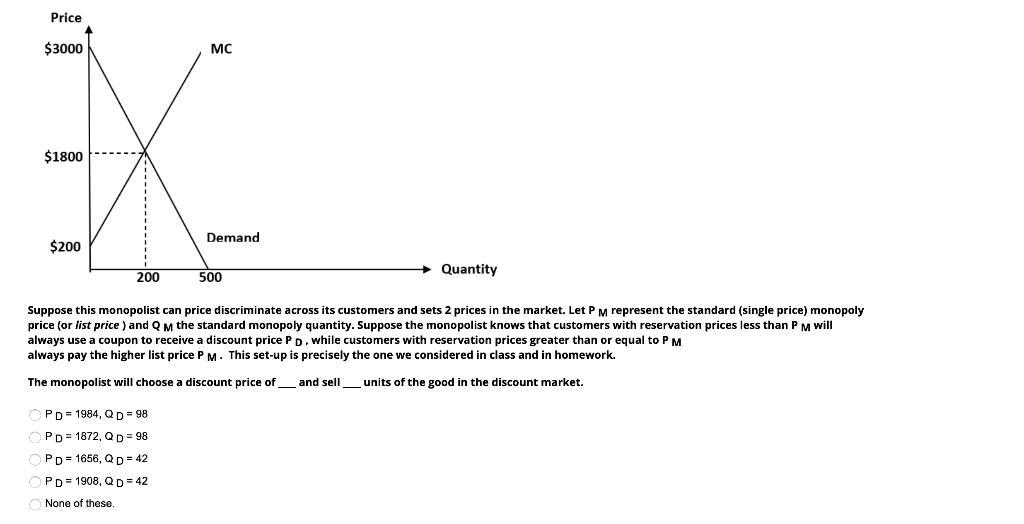

Answer:

hello your question is incomplete attached below is the missing part

answer: Pd = 1658 , Qd = 42

Explanation:

The monopolist will choose a discount price of ( Pd ) = 1658 and sell 42 units of the good in the discount market

since the standard price is at $1800 and the Qm ( standard monopoly quantity) is at 200 for the Monopoly to be profitable the amount of good to be sold to customers with reservation prices greater than or equal to standard price should be greater than the good offered at discount price and also the discount price after using a coupon should be lower than the standard price (Pm)

Answer:

Earning Satisfactory Profits

Explanation:

Based on the information provided within the qeustion it seems that the management of Fresnas Designs Inc. bases its pricing policy on Earning Satisfactory Profits. This is basically when a company revolves all their decisions around trying to make a reasonable level of profits that is consistent with the level of risk that they face. Which is what Fresnas is doing by pricing their products reasonably as opposed to pricing them higher even thought hey can.

Answer:

price level fall and value of money is rises

Explanation:

given data

one year basket costs = $10.00

two year two basket costs = $9.00

one year buy baskets = $50

year two,buy baskets = $50

to find out

as the price level falls, the value of money will be

solution

we see that when we compare to 1 year price go down from $10 to $ 9

so deflation at annual rate is  = 10%

= 10%

so here

sum of $50 will be buy here =  = $5 in one year

= $5 in one year

and $ 50 buy in 2 year is =  = $5.56 in two year

= $5.56 in two year

so this is show here that price level fall and value of money is rises