Answer:

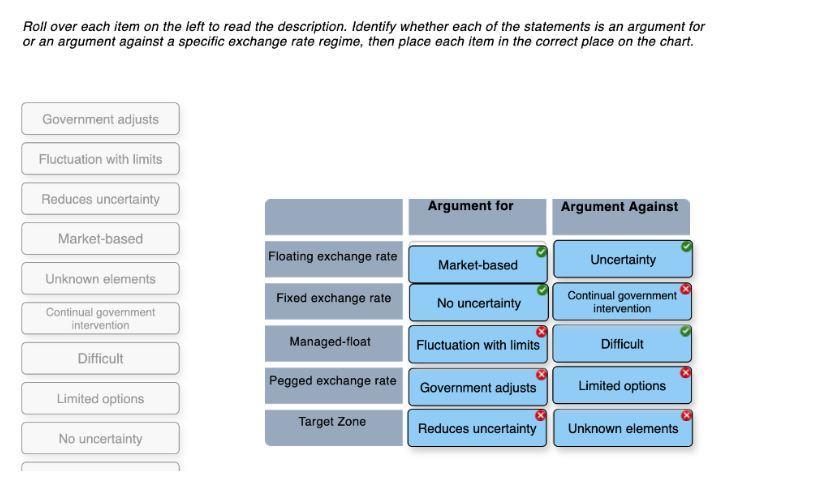

<u>Floating exchange rate</u>

Here the market decides the value of the currency as it trade freely in the market based on supply and demand.

Argument For;

Market Based - It is market based therefore it reflects the true value of the currency.

Argument Against;

Uncertainty - As it trades according to the whims of supply and demand, telling which direction it will go in terms of value is a difficult undertaking therefore financial decisions based on such are riskier.

<u>Fixed exchange rate</u>

Here the value of the currency is fixed either to the value of another currency or to the price of gold.

Argument For;

No Uncertainty - As the currency is tied to another currency which is usually more stable or gold, the rate of the currency is more predictable.

Argument Against;

Unknown Elements

<u>Managed float</u>

In this exchange rate regime, the Central bank of a country intervenes in the Foreign exchange market to push or pull the currency in the direction that it prefers.

Argument For;

Government intervention - The Government Intervention ensures that the currency's value remains stable as well as allowing the Central bank to maintain a good balance of payments.

Argument Against;

Difficult - Maintaining the currency within the band preferred in a difficult undertaking that requires constant intervention in the Forex market.

<u>Pegged exchange rate</u>

The Central bank in this instance pegs the currency to a basket of currencies after setting an exchange rate it would prefer and then intervenes in forex market to keep it that way.

Argument For;

Reduces uncertainty - The movement of the currency is more predictable due to it being pegged to a basket of currencies.

Argument Against;

Continual government intervention - As this requires the currency to remain at a certain value, the government will keep intervening to ensure that it stays at that exact level.

<u>Target zone</u>

Here the Central Bank allows the currency to fluctuate on the market albeit with limits placed on how much it can do so.

Argument For;

Fluctuation with limits - By combining fixed regimes with floating regimes, the currency can maintain a semblance of true value whilst still be less uncertain.

Argument Against;

Limited options.