If a production quota is set lower than the equilibrium quantity, at the quota quantity, the marginal benefit is greater marginal cost and the quantity produced is allocative greater.

If marginal benefit exceeds marginal cost, resources use will be more efficient if the quantity is increased. If marginal cost exceeds marginal benefit, resource use will be more efficiently if the quantity is increased.

Allocative efficiency occurs where the collective sum of consumer and producer surplus is at a maximum. When the marginal benefits exceed the marginal costs of producing a product, then allocative efficiency is not achieved in the market.

Learn more about equilibrium quantity at

brainly.com/question/22569960

#SPJ4

It is the amount of interest paid on the unpaid balance. Its the fee you're charged for financing the debt.

Answer:

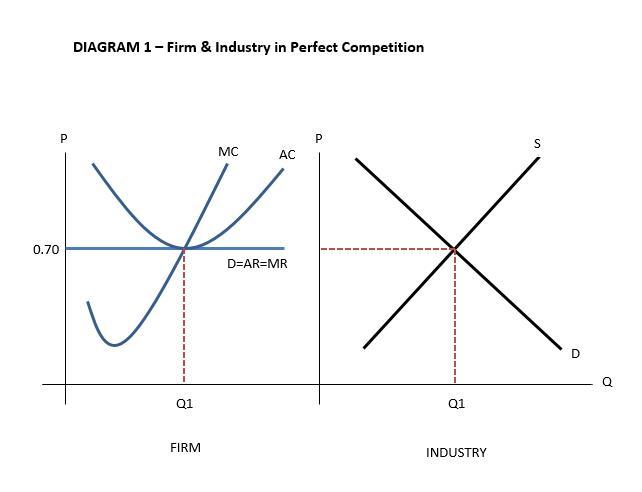

Refer explanation and diagrams

Explanation:

1. The ranching industry exists in the perfectly competitive market where there is ease of entry and exit into and out of the market, as well as many suppliers producing homogeneous products. At an equilibrium of 70 cents per pound, suppliers will be making normal profits, selling at Q1 where the AC, MC and D=AR=MR curves meet (Refer Diagram 1).

2. When feed costs are cut by 27%, it means that the cost of production of these firms will fall. Due to this, the AC curve will shift lower to AC1. At this point, the firms in the ranching industry would be making supernormal profits in the short-run of the area shaded in the diagram (Refer Diagram 2).

3. In the long run, seeing these super normal profits, new firms would be encouraged to enter into the market. The ease of entry nature of perfect competition will result in the supply curve shifting from S to S1. Hence, industry equilibrium quantity moves from Q1 to Q2. This causes a fall in price from 70 cents to Pe. Thus, in the long-run, firms will go back to producing at normal profits once again. (Refer Diagram 3).

Answer:

generally $1,000, but some policies can cover up to $1,250

Explanation:

Home insurance provides only very limited protection to boats or other watercraft that you might own. They are also very specific circumstances under which they will be covered and as long as it happens within your residence. In this case, since the boat trailer was stolen from your driveway you insurance policy will probably cover it, but the amount is relatively small. Most policies will cover only $1,000 and some might even cover up to $1,250, but generally the lesser amount is covered. If you own a boat it is usually recommended to get a boat insurance policy.

The answer is online surverys!! Hope this helps