Answer:

C. $13,356

Explanation:

Evan, a shareholder, owned 20% of Yorker's stock for 200 days and 25% of Yorker's stock for the remaining 165 days of the year (not a leap year).

Using the required per-day allocation method, Evan's share of the S corporation's ordinary income of $60,000 (rounded to the nearest dollar) is:

0.2 x 60,000 x (200 / 365) + 0.25 x 60,000 x (165/365) = $13,356.16

Answer: D. I, II, and III

Explanation:

If expecting a price deduction, you can buy Put options. These give you the right to sell an underlying stock at a certain price regardless of what the price in the market is. If you purchased this, you can sell your stock above market value if it does go down.

You can sell write call options for a fee where you give the buyer the right to buy your shares at a certain price in future. This is only valuable if prices rise so as you are expecting prices to fall, you could make a premium on the call option contract fees if prices fall without having to sell off your shares.

Hedging with puts is better than short calls if you are expecting a major stock price decline as the opportunity for profit is higher.

Explanation:

As an online university, UoPeople assists in the strategic knowledge that the university student will use in his professional life. The most useful strategy learned was that of time management. It is important to know how to manage the time to carry out the online education curriculum and the activities carried out offline in order to achieve the objectives defined effectively.

Therefore, through time management, there is the possibility of greater organization of academic and social life, as well as increased motivation.

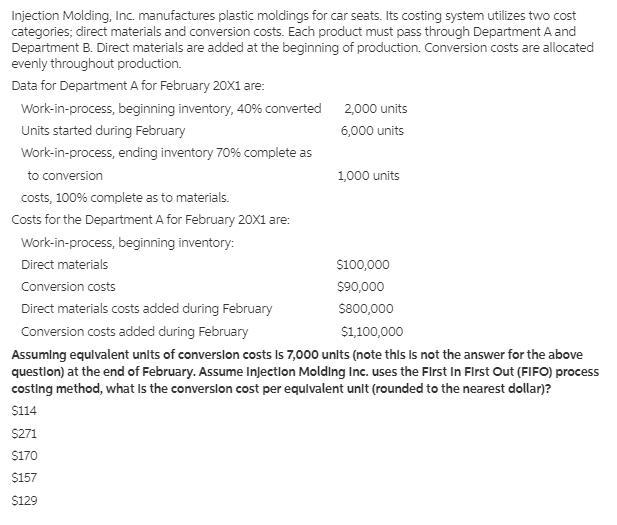

Answer:

$157 per equivalent unit

Explanation:

Note: <em>The full question is attached as picture below</em>

<em />

Conversion cost per equivalent unit = Conversion costs added during February / Equivalent units of conversion costs

Conversion cost per equivalent unit = $1,100,000 / 7000 units

Conversion cost per equivalent unit = $157.14286

Conversion cost per equivalent unit = $157 per equivalent unit

Answer:

horizon value at year 5 = Div₆ / (Re - g)

- Div₆ = ($2.75 x 1.143²) x 1.0372 = $3.726384483

- Re = 12.4%

- g = 3.72%

horizon value at year 5 = $3.726384483 / (12.4% - 3.72%) = $42.93

current value P₀ = $2.75/1.124³ + $3.14325/1.124⁴ + $46.52273/1.124⁵ = $1.937 + $1.969 + $25.932 = $29.838 ≈ $29.84

1) dividend yield = 0/$29.84 = 0%

capital gains yield = (P₁ - P₀) / P₀

P₁ = $2.75/1.124 + $3.14325/1.124² + $46.52273/1.124³ = $2.447 + $2.488 + $32.762 = $37.697 ≈ $37.70

capital gains yield = ($37.70 - $29.84) / $29.84 = 26.34%

2) Goodwin has yet to record a profit (positive net income). Is this statement a possible explanation for why the firm hasn't paid a dividend yet?

A. Yes

Since dividends must be paid out from net profits or retained earnings.