A 401(k) is a good long-term investment strategy hope it helps

Answer:

The correct answers are:

- Debt.

- An IOU promise to pay.

- The stockholders.

Explanation:

To begin with, in the field of finance the <em>bond</em> is an instrument of <u>indebtedness</u> of the bond issuer to the holders. Moreover, this instrument is also known as a <u>debt security</u> under which the party that generated the bond owes a debt to the holder of the bond and must pay ir under certain circumstances stipulated at the time of the purchase, therefore that it is known that the bond is a form of<u> ''I owe you'' or IOU</u> promise to pay. Furthermore, the <u>bondholders are only lenders</u> and therefore they do not owe a part of the company, so that means that if the company runs into financial difficulty then the stockholder, who do owe a part of the company, will be paid first.

Answer:

Services

Explanation:

In the game of economics, services are actions that other people value. Services are something which people get and it helps to improve the utility level of a customer. Services are valued by people because it satisfies their needs and wants. Moreover, this is why people pay a lot of money to get better services because it plays an important to fulfil human wants.

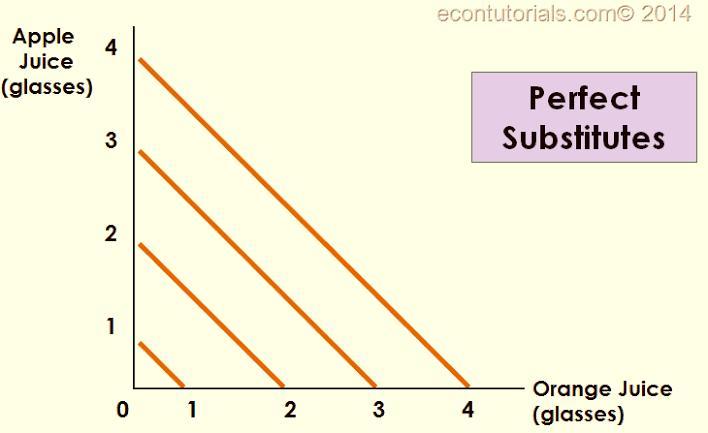

Answer:

The isoquants will be straight parallel lines.

Explanation:

In the given secanrio copper or bronze may be used to produce jewellery. The utility derived from use of either one is the same. They are perfectly interchangeable. Therefore copper and bronze are perfect substitutes.

The isoquant curve shows all combinations of input that can be used to produce units of output.

For goods that have perfect substitution the isoquants are straight lines that are parallel to each other. The marginal rate of technical substitution is 1, and isoquant have slope angle of 45° with each axis.

Find attached an illustration of this. So copper is a perfect substitute for bronze.

Answer:

Explanation:

No, He deserves a peaceful inauguration.