Answer:

The correct answer is B,false

Explanation:

Opportunity cost is naturally the cost of alternative forgone,that is the benefits ignored as a result of taking a particular course of action.

Obviously,the opportunity cost of the bouffe to Betty is the practicing calculus problems for her math examination that she could not partake in.

The opportunity cost would only be the practicing session missed if Betty was able to pass the examination,otherwise the opportunity becomes bigger if she fails the exam to include the costs of paying and preparing for another examination

Answer:

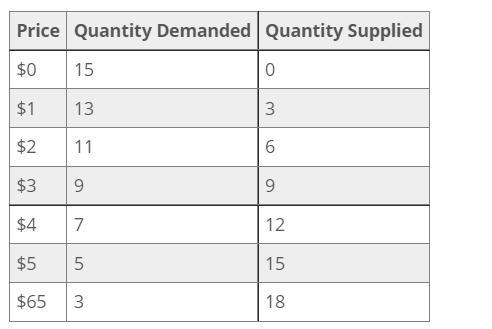

$3

Explanation:

A price floor is when the government or an agency of the government sets the minimum price of a product. A price floor is binding if it is set above equilibrium price.

Price ceiling is when the government or an agency of the government sets the maximum price for a product. It is binding when it is set below equilibrium price.

Equilibrium price is the price at which quantity demand equal quantity supplied. Above equilibrium price there is a surplus - quantity supplied exceeds quantity demanded.

Below equilibrium price there is a shortage - quantity demanded exceeds quantity supplied

Shortage = $12 - $9 = $3

Answer:

The total dollar return per share is 11% or $3.7

Explanation:

Total dollar return = (Selling price- buying price + total dividend)/buying price.

The buying price is 32.50

The selling price= 34.60

The total dividends are 0.4*4=1.6 because in 1 year there will be 4 quarterly dividends.

Now we input these numbers in a formula

(34.60-32.50+1.6)/32.50=0.11

= 11%

In dollar terms the return is

34.60-32.50+1.6=3.7

Answer:

correct option is C. $250,000

Explanation:

given data

sold the home and gain = $300,000

to find out

amount of the gain allowed to exclude from gross income

solution

we know that Michael owned the property for the 10 years

so here Michael is not allowed to exclude the gain = 10 % that is $30,000

and The maximum gain exclusion permitted = $250000

so here Michael will recognize $50,000 because amount exceed $250,000 for a single taxpayer and exclusion of gain on sales of property tax payer need to own and occupy the property as principle residence for the 2 out of 5 year immediately preceding the sales

so here correct option is C. $250,000