Answer:

2865.09

Explanation:

V0 = #Shares * Price per Share

V0 = 100 * 25.8 = 2580

V1 = Today´s Value

V1 = 2865

Return Year 1 = (V1 - V0) / V0

Return Year 1 = (2865 - 2580)/2580

Return Year 1 = 11.05%

New Investment

Abby's desire is to get the same return of 11.05%. So for the next year her investment should be 2580 * (1 + return) --> 2580 * (1 + 0.1105) = 2865.09.

Remember that we are assuming that the 50 are part of the purchase price and we are assuming that she did not add any money.

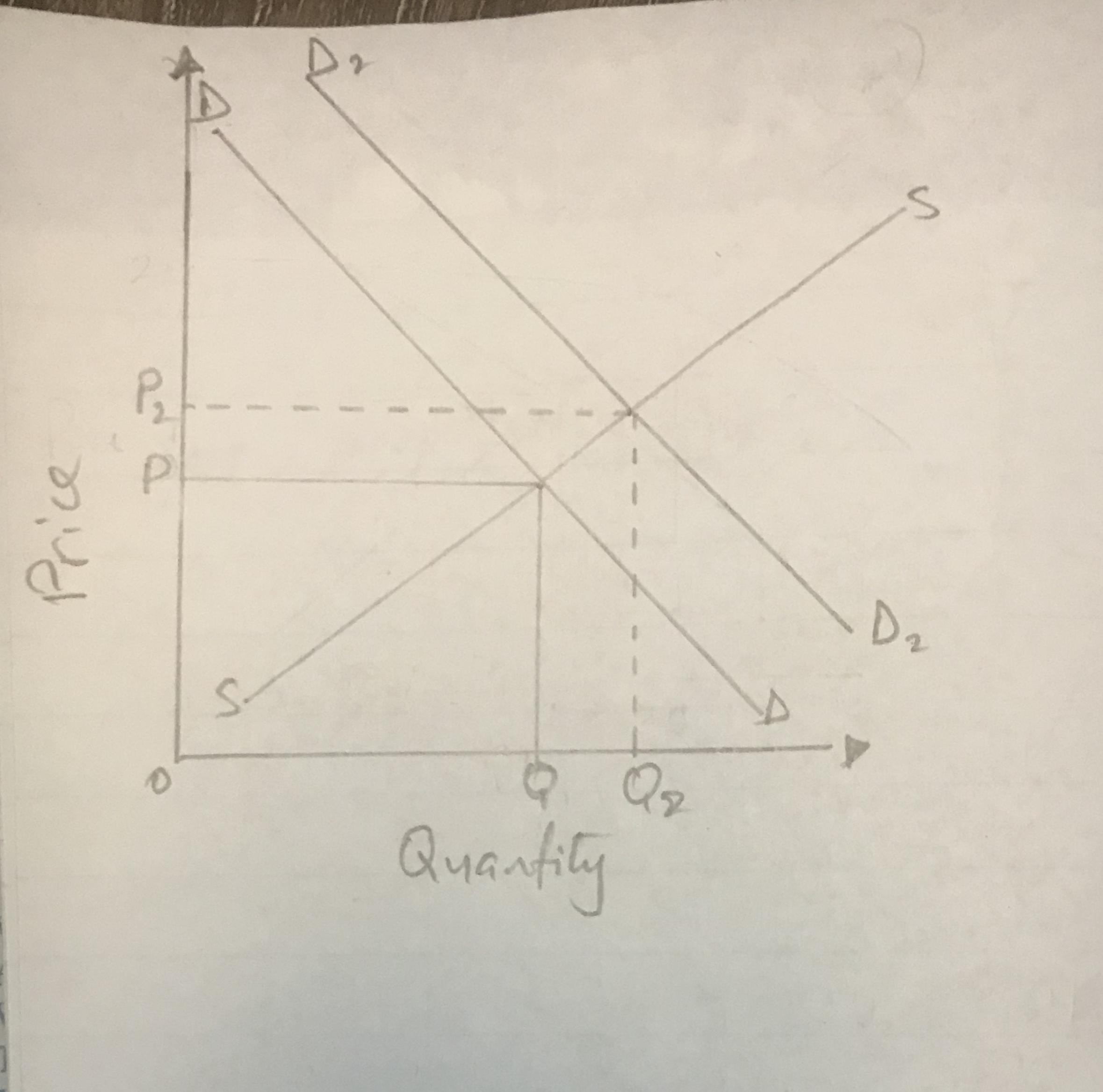

Answer: The correct answer is option B; Add D2 to the right of D, showing an increase in demand and increase in equilibrium price.

Explanation: The demand for a commodity is usually affected either positively or negatively by some factors or determinants. Foremost among the factors of demand is price of the commodity. Other factors include;

(a) Price of substitute commodities

(b) Consumers preferences

(c) Population

(d) Weather conditions

(e) Advertising

In the question above, the use of a popular actor as the spokesperson of the product is a form of advertising that is intended to improve upon the perception of the commodity and hence encourage consumers to buy more of it. If the popular personality endorses a product, there is an almost one hundred percent likelihood that consumers would see the product as a preferred choice and this would cause the demand to go up or increase.

An increase in the market demand would be signified by the outward shift of the demand curve to the right from D to D2. Since the x-axis shows the quantity demanded increasing towards the right hand side, then an increase in market demand would be reflected by a shift of the demand curve to the right.

As a result of that, the price would now move from P to P2 which shows an increase in equilibrium price. Also the quantity demanded would move from Q to Q2 which also indicates an increase in demand.

Answer:

Sunk cost. The individual is still considering sunk cost in making future decisions

Explanation:

Sunk cost is cost that has already been incurred and cannot be recovered. It should not be considered in making future decisions.

In this question, the money paid for the meal is the sunk cost and it shouldn't be considered in making the decision of whether to continue the meal or not to.

I hope my answer helps you

Answer:

$75,600

Explanation:

We divide the total sales with the number of units to get the unit price . Similarly we get the unit price for the variable costs. But as the fixed costs remain constant they will not change. We get the contribution margin =$75,600

Lasseter Corporation

Contribution Format Income Statement for August

Sales (4,200 units) $ 127,100 /4100= $31 * 4200 $ 130200

Variable expenses (53,300/4100)*4200 = $ 54600

Contribution margin 75,600

Fixed expenses 44,200

Net operating income $ 31,400

Lasseter Corporation

Contribution Format Income Statement for August

Sales (4,100 units) $ 127,100

Variable expenses 53,300

Contribution margin 73,800

Fixed expenses 44,200

Net operating income $ 29,600

Answer:

B. Search Ads 360

E. Display & Video 360

Explanation:

Other than Search Ads 360 and Display & Video 360 all other mentioned products are available in the Small business version of Google Marketing Platform.