Answer:

The monthly payment will be = $5161.08

The final payment will be: = $413,684.38

Explanation:

From the given information:

Given that:

the loan amount = $521000

The interest rate for the loan is = 8.6% compounded monthly

the loan is being amortized for 15 years

Thus, the firm will be paying the due amount after 15 years

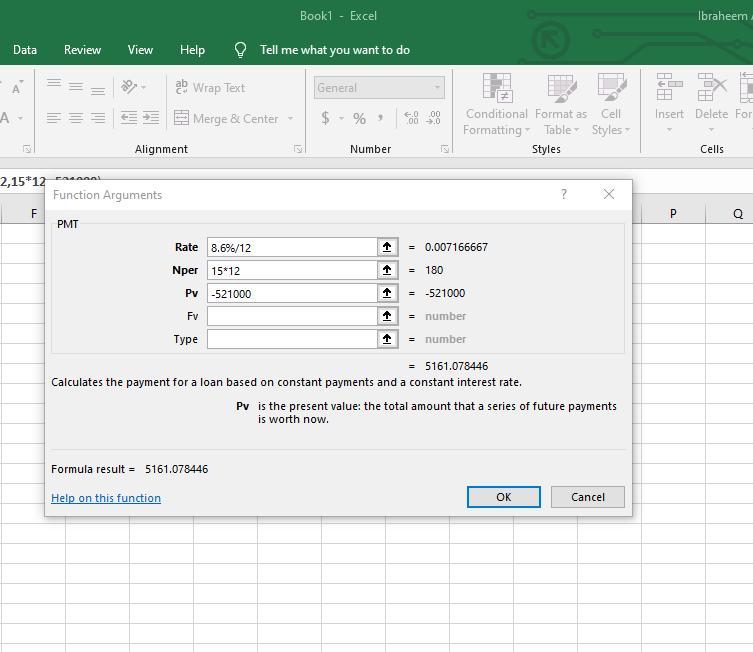

We use the Excel software to find the monthly payment and the final payment.

a. Using the Excel Function ( =PMT(8.6%/12,15*12,-521000) )

The monthly payment will be = $5161.08

b.Using the Excel Function (=CUMPRINC(8.6%/12,15*12,521000,60,180,1) )

The final payment will be: = $413,684.38

These can be seen in the images attached below.