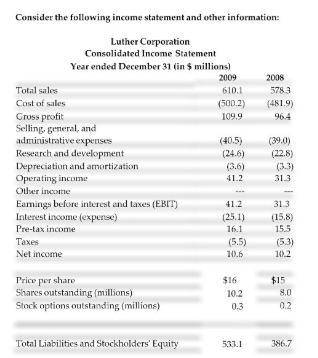

Answer:

the operating margin is 5.4%

Explanation:

The computation of the operating margin is shown below:

As we know that

Operating Margin = Operating Income ÷ Sales

= $31.3 ÷ $578.3

= 5.4%

Hence, the operating margin is 5.4%

It could be determined by dividing the operating income from the sales

Gloria Jean’s Coffees

Caribou Coffee

peets coffee

Coffee Beanery

Dunkin’ Donuts

Costa Coffee!

Answer:

<em>A. autoworker who is temporarily laid off from an automobile company because of a decline in sales.

</em>

Explanation:

Cyclical unemployment is <em>unemployment that occurs when full employment can not be met by the aggregate demand for goods and services in an economy.</em>

This takes place during times of decreased economic growth or times of economic slowdown.

Cyclical unemployment is directly linked to the degree of macroeconomic behavior, which is the combined or collective activity of all economically involved individuals and entities.

Instead of linear, this overall trend is cyclical-economic activity tends to increase and fall rather than always rising or falling.

Answer: "marketing strategy" .

____________________________________________________

Answer:

It is the sum of the inventory held across all of the locations in a company.

Explanation:

Total system inventory is a business term that is used in describing the total sum of the inventory held by a particular company across all of the locations in which that company is situated regardless of whether vacant or rented.

Hence, in this case, the correct answer is option B