Answer:

Option A) $5000

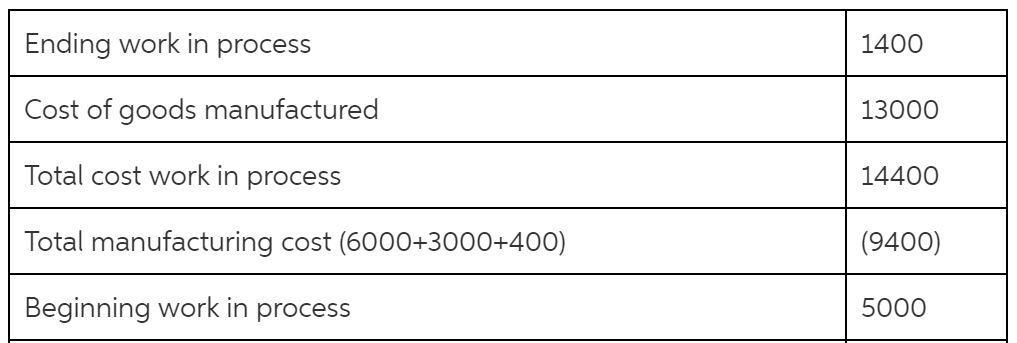

Explanation:

The explanation for this question is given in the attachment below.

Answer:

Yes

Explanation:

Because of he really wants to sees his company growing up to another level

<span>The answer is C. Postsecondary alternatives are differed and may incorporate open or private colleges, universities, junior colleges, profession/specialized schools, professional/exchange schools, habitats for proceeding with instruction, grounds progress projects, and apprenticeship programs.</span>

The trend toward hiring temporary workers is up.

Answer:

product mixes include product lines.

Explanation:

The product line is a group of products that are interrelated as they satisfy the needs and also they are used together and are sold to the similar customer group via similar outlets

It involved the product line that are offered by the company

Therefore according to the given situation, last one is correct answer

And, the same would be relevant