Answer:

Please see the calculation explanation below and the depreciation expense chart for all methods is attached.

Explanation:

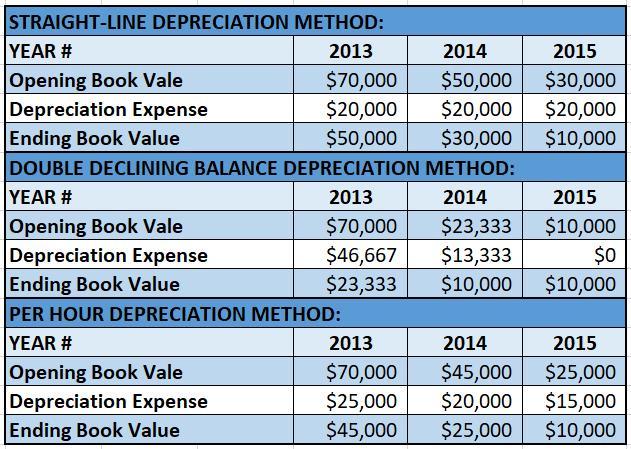

1. STRAIGHT-LINE DEPRECIATION METHOD:

<em>Depreciation Expense = (Total Cost - Residual Value) / Useful Life

</em>

Depreciation Expense = ($70,000 - $10,000) / 3 years

Depreciation Expense = $60,000 / 3 years

Depreciation Expense = $20,000 per year

2. DOUBLE DECLINING BALANCE DEPRECIATION METHOD:

<em>Depreciation Expense Rate = (100% / Useful Life) x 2

</em>

Depreciation Expense Rate = (100% / 3) x 2

Depreciation Expense Rate = 66.67%

<em>2013:

</em>

Depreciation Expense = $70,000 x 66.67% = $46,667

<em>2014:

</em>

Depreciation Expense = ($70,000 - $46,667) x 66.67% = $15,556

Since the residual value is $10,000 and as per Double Declining Balance Method, the point at which Book Value is equal to the residual value, no depreciation is taken.

<em>Depreciation Expense = (Total Cost - Residual Value) - (Accumulated Depreciation)

</em>

Depreciation Expense = ($70,000 - $10,000) - ($46,667)

Depreciation Expense = $13,333

<em>2015:

</em>

No Depreciation Expense for year 3, as Book value is already equal to residual value in year 2.

3. PER HOUR DEPRECIATION METHOD:

<em>2013:</em><em>

</em>

<em>Depreciation Cost per hour = (Engine Hours in 2013 / Total Engine Hours) x (Total Cost - Residual Value)

</em>

Depreciation Cost per hour = (500 / 1,200) x ($70,000 - $10,000)

Depreciation Cost per hour = $25,000

<em>2014:

</em>

<em>Depreciation Cost per hour = (Engine Hours in 2014 / Total Engine Hours) x (Total Cost - Residual Value)

</em>

Depreciation Cost per hour = (400 / 1,200) x ($70,000 - $10,000)

Depreciation Cost per hour = $20,000

<em>2015:

</em>

<em>Depreciation Cost per hour = (Engine Hours in 2015 / Total Engine Hours) x (Total Cost - Residual Value)

</em>

Depreciation Cost per hour = (300 / 1,200) x ($70,000 - $10,000)

Depreciation Cost per hour = $15,000