Answer and Explanation:

For computing the present value we need to apply the present value formula i.e to be shown in the attachment

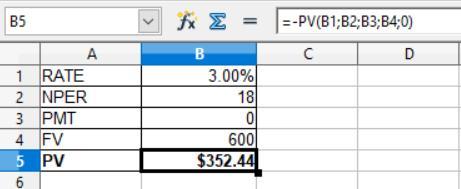

For the first case i.e semi annual compounding

Given that,

Future value = $600

Rate of interest = 6% ÷ 2 = 3%

NPER = 9 years × 2 = 18 years

PMT = $0

The formula is shown below:

= -PV(Rate;NPER;PMT;FV;type)

So, after applying the above formula, the present value is $352.44

For the second case i.e quarterly compounding

Given that,

Future value = $600

Rate of interest = 6% ÷ 4 = 1.5%

NPER = 9 years × 4 = 36 years

PMT = $0

The formula is shown below:

= -PV(Rate;NPER;PMT;FV;type)

So, after applying the above formula, the present value is $351.05

For the third case i.e monthly compounding

Given that,

Future value = $600

Rate of interest = 6% ÷ 12 = 0.5%

NPER = 1 years × 12 = 12 years

PMT = $0

The formula is shown below:

= -PV(Rate;NPER;PMT;FV;type)

So, after applying the above formula, the present value is $565.14

Based on the various compounding i.e semi annual, quarterly and yearly the present value would be different in each case