I think for Japan CDs

And for Canada Beef

Answer:

b. 60%

Explanation:

The computation of percentage is assigned to Cost of Goods Sold is shown below:-

$ %

Sales $300 $100

Cost of Goods Sold $180 $60 ($180 ÷ $300) × 100

Gross Profit $120 $40 ($120 ÷ $300) × 100

Operating Expenses $45 $15 ($45 ÷ $300) × 100

Net Income $75 $25 ($75 ÷ $300) × 100

Percentage assigned to cost of goods sold = Cost of goods sold ÷ Sales × 100

= $180 ÷ $300 × 100

= 60%

Therefore for computing the percentage is assigned to Cost of Goods Sold we simply applied the above formula.

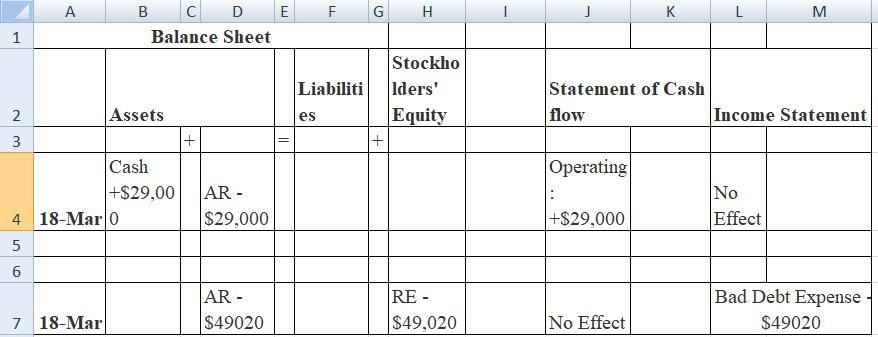

Answer and Explanation:

The effect of the given transaction is shown in the attachment below. Please find the attachment

As we know that

Accounting equation is

Total assets = Total liabilities + total stockholder equity

So,

1. In the first transaction there is an increased in assets by $29,000 and decreased the assets by $29,000 plus the same is to be recorded in the operating section of the cash flow statement

2. In the second transaction, there is decreased in asset for $49,020 also the retained earning is also decreased by same amount plus there is a bad debt expense also

Answer:

$5.50 dividend per share to common stock

Explanation:

In case a company has cumulative preference shares then the company has to pay preference dividend in arrears

Here, preference dividend was not paid in the year 2017

Preference dividend for 2017 = 500  $100 4%

$100 4%

= $2,000

Since the dividend is paid in between the year 2018, dividend is paid for the year 2017 and not for 2018 thus preference dividend is for a year, only for 2017

Therefore, dividend to common equity = $35,000 - $2,000 = $33,000

Dividend per share = $33,000/6,000 = $5.50 per share

Answer:

Consider the following explanation.

Explanation:

The six different strategies (spreads or combinations) the investor can follow:

1)short Butterfly spread: it’s a spread with selling one call option with the lowest strike price(XL),purchasing two call options with the medium strike price(XM) and selling one call option with the highest strike price (XH) , XL<XM<XH. The strike price (XM) is generally chosen such that its equal to the stock price and options are of same maturity. The strategy shall generate the net income from the selling of calls when the stock price deviated from the strike price XM due to the high volatility. A high jump either way guarantees a net income.

2) The Straddle combination with long one put and long 1 call with the same strike price X and maturity. Its payoff depends on the deviation of the strike price if the big jump either way is expected then either the put or the call expires in the money so that the moneyness(payoffs) covers all the premiums paid for the call and put and there are profits. The high jump either way guarantees a big payoff from either the put or the call.

3)In the Strangle combination there is one long call with strike price (Xc) and one long put with strike price Xp,this combination is cheaper to generate due to purchase of OTM(out of the money) options. If the big jump either way is expected then either the put or the call expires in the money so that the moneyness (payoffs) covers all the premiums paid for the call and put and there are profits. The high jump either way guarantees a big payoff from either the put or the call. It’s easier to cover all the lesser premiums paid for the call and put and generate profits with a big move.

4) The Strip combination consists of 1 call+2 put with same exercise price and maturity. If the big jump either way is expected then either the two put or the call expires in the money so that the moneyness covers all the premiums paid for the call and put and there are profits. The payoff generated by the 2 puts is much more when the stock moves downwards as compared to when the stock moves upwards. Investor is sure of the uncertain directional big jump but thinks that the probability of downward move is greater than the upward move.

5) The Strap combination consists of 2 calls+1 put with same exercise price and maturity. If the big jump either way is expected then either the 1 put or the 2 calls expires in the money so that the moneyness covers all the premiums paid for the call and put and there are profits. The payoff generated by the 2 calls is much more when the stock moves upwards as compared to when the stock moves downwards. Investor is sure of the uncertain directional big jump but thinks that the probability of upward move is greater than the downward move.

6) Short Calendar spread: short shorter term call and at the same time short longer term call therefore the income is generated by the big move from the premiums of the calls and differences in the maturity.