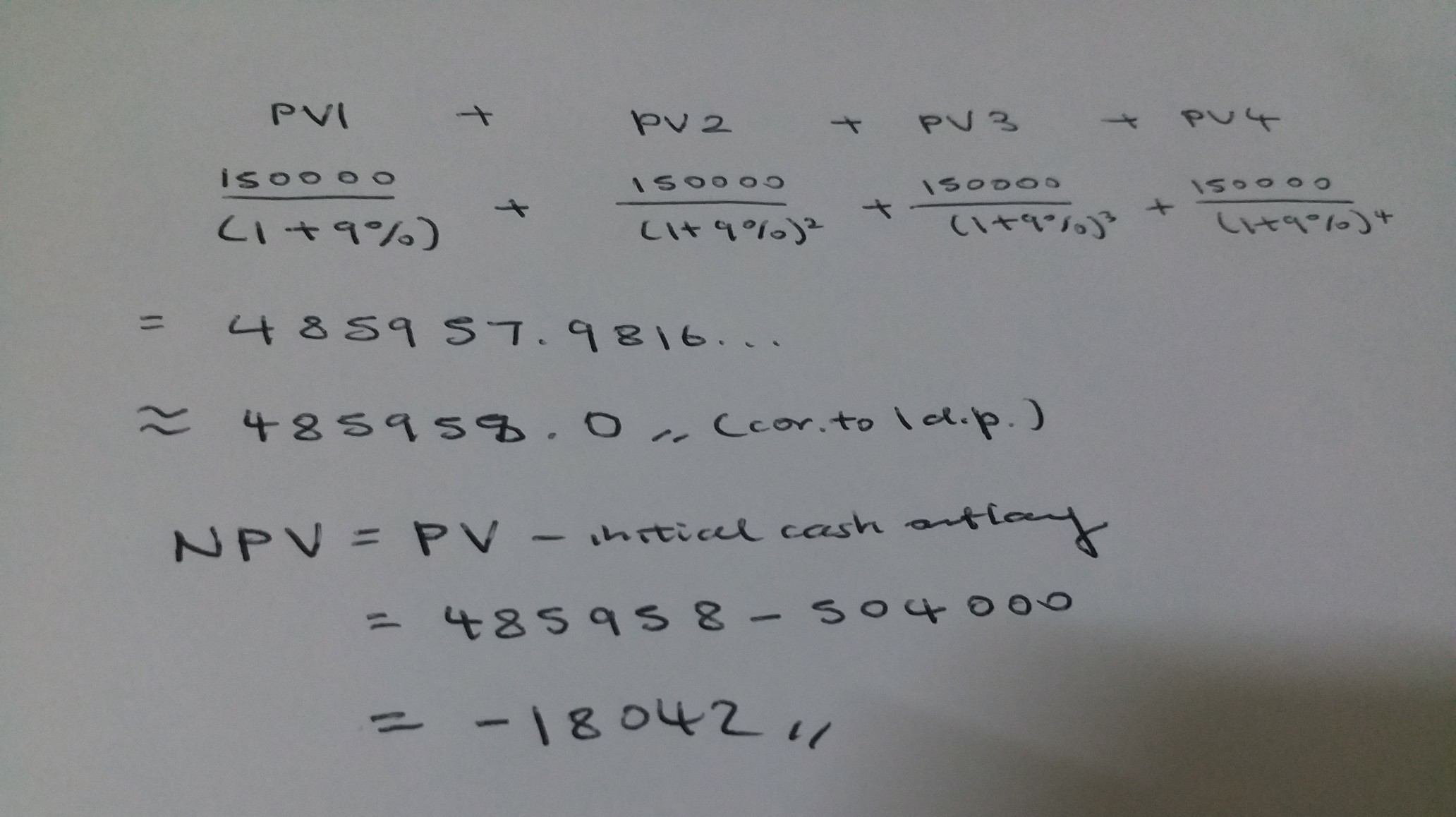

Answer: $67600

Explanation:

Using the flow-to-equity method of valuation, the amount borrowed will be calculated thus:

NPV = $157000

Add : Initial investment = $640000

Present value of cash inflow = $797000

Less : Present value of Levered cash flow = $729400

Amount borrowed = $67600

Therefore, the amount borrowed is $67600.

It is true because I said it is and because it is true and I am not wrong because everything I say is true

<span>The Arizona jean co. brand of jeans, owned by J.C. Penney, is a private label brand. The private brand is exclusive to that retailer (for example </span>carries the retailer’s name) but is produced by another company.<span> Consumers choose private brands because they tend to be lower in price than their counterparts. </span>

Dr. bills Payable 6300 Notes Payable 6,300.

The journal entry used for recording the issuance of a note for the cause of converting a current account payable could be to debit the bills payable and credit the notes payable.

A magazine entry is a record of an enterprise transaction for your business books. In double-access bookkeeping, you're making at least two journal entries for each transaction. Because a transaction can create a variety of changes in a commercial enterprise, a bookkeeper tracks them all with magazine entries.

An example of a journal is a diary in which you write about what happens to you and what you are wondering. An example of a journal is the brand new England journal of drugs, wherein new studies are posted which are relevant to docs and medicinal drugs.

Magazine entry format is the usual layout utilized in bookkeeping to maintain a record of all of the organization's business transactions and is especially based totally on the double-access bookkeeping device of accounting and guarantees that the debit aspect and credit facet are usually the same.

<em>The question is incomplete. Please read below to find the missing content.</em>

The journal entry to record the conversion of a $6,300 accounts payable to notes payable would be

A: Cash 6,300

Notes Payable 6,300

B: Notes Receivable 6,300

Notes Payable 6,300

C: Notes Payable 6,300

Cash 6,300

D: Accounts Payable 6,300

Notes Payable 6,300

Learn more about the journal entry herehttps://brainly.com/question/14279491

#SPJ1