Answer:

Check the explanation

Explanation:

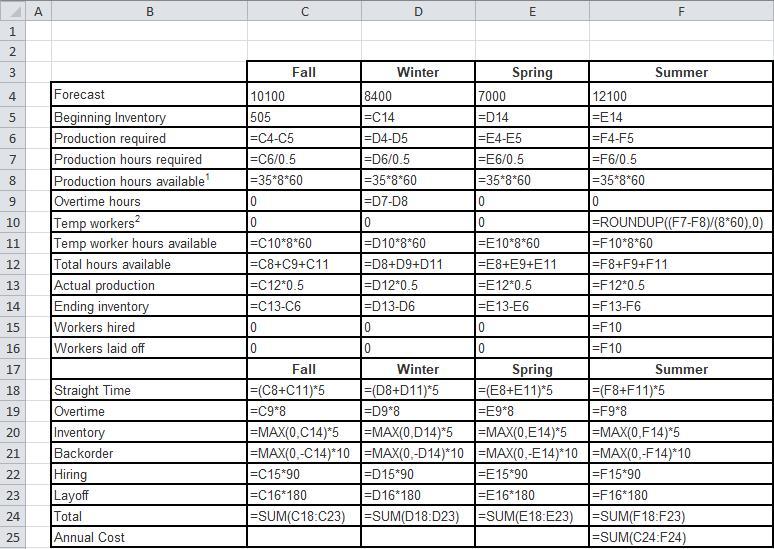

Fall Winter Spring Summer

Forecast 10,100 8,400 7,000 12,100

Beginning Inventory 505 -1,195 0 1,400

Production required 9,595 9,595 7,000 10,700

Production hours required 19,190 19,190 14,000 21,400

Production hours available1 16,800 16,800 16,800 16,800

Overtime hours 0 2,390 0 0

Temp workers2 0 0 0 10

Temp worker hours available 0 0 0 4,800

Total hours available 16,800 19,190 16,800 21,600

Actual production 8,400 9,595 8,400 10,800

Ending inventory -1,195 0 1,400 100

Workers hired 0 0 0 10

Workers laid off 0 0 0 10

Fall Winter Spring Summer

Straight Time $84,000 $84,000 $84,000 $108,000

Overtime 0 $19,120 $0 $0

Inventory $0 $0 $7,000 $500

Backorder $11,950 $0 $0 $0

Hiring $0 $0 $0 $900

Layoff $0 $0 $0 $1,800

Total $95,950 $103,120 $91,000 $111,200

Annual Cost $401,270

kindly check the calculation in the image below.