Answer:

broad reach and mobility

Explanation:

Mobile computing refers to all types of devices that allow access to information regardless of the individuals' location. Laptops, smartphones, tablets, handle gaming devices, and wearable devices are part of mobile computing.

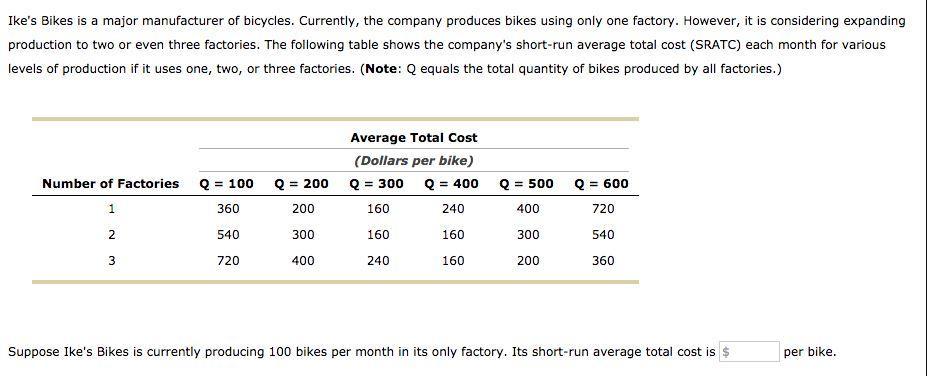

The short-run average total cost of Ike's Bikes of producing 100 bikes is $360.

<h3>

What is the short-run average total cost ?</h3>

The short-run is a production period where some of the factors used in the production process are fixed and others are variable. The short-run average total cost is the total cost divided by total output. Total cost is the sum of fixed cost and variable cost.

Please find attached the complete question. To learn more about average cost, please check: brainly.com/question/26959638

Answer:

The amount of cash received will be $6039

Explanation:

The amount of cash received on January 24 will be the net amount after deducting the sales returns and the discount allowed as the payment is made within 10 days period of the sale and the terms 1/10 states a 1% discount if payment is made within 10 days.

The net value of receivables after sales returns = 7000 - 900 = 6100

The discount allowed = 6100 * 1% = 61

Cash to be received = 6100 - 61 = $6039

:0

yas I will vote him!

lol

wait..no! He will just take our money. My answer is a maybe.

Answer:

land 45,000 debit

building 95,000 debit

common stock 100,000 credit

additional paid-in 40,000 credit

--issuance of shares in exchange of land an the building on it--

Explanation:

common stock face value:

10,000 shares x $10 = $100,000

fair value of the acquired assets:

land 45,000

building 95,000

total 140,000

Additional paid-in calculation

140,000 recieved for the shares

<u> - 100,000 </u>

40,000 additional paid-in

We consider the face value as the incurred cos t five years ago are not relevant today. The land and building are appraised at their market value