Answer:

A) $15.50

Explanation:

MC = Change in Total cost / Change in output

The marginal cost of walking that 26th dog is = ($315.50 - $300) / (26 -25)= $15.50 / 1 = $15.50. So, Option A is the correct option

Answer:

- A

- E

- B

Explanation:

1) consolidated balance for the equipment account as of December 31 2018

Goehler equipment with book value = $975000

Kenneth equipment with book value = $105000

purchase price allocated to Kenneth's equipment = $30000 ( 120000 - 90000)

Amortization of allocation = purchase price allocated to Kenneth * 2 / 10

= (30000 * 2) / 10 = $6000

therefore consolidated balance = 975000 + 105000 + 30000 - 6000

= $1,104,000

2) applying partial equity method in accounting ( the consolidated balance will be )

The same procedure used in calculating for question 1 is applicable to partial equity method of accounting hence the answer will be the same

= $1104000

3) applying the initial value method in accounting for Kenneth

- The same procedure used in calculating the partial equity procedure is applicable to initial value procedure hence the answer will be = $1104000

Answer: C. inefficiently low; inefficiently high

Explanation:

If the cotton farmers are not made to pay for the damage that their pesticides cost then they will maintain production at a relatively high level because their input costs will be relatively low. As a result of this high level of production, the price of the goods will be relatively low as well. The point at which both market equilibrium quantity and price are at in this scenario are considered inefficient because they are not taking into account, the true cost of production being the effects of the pesticides being used.

However, if they are made to pay for this negative externality that they are the cause of, it will increase their production cost and force them to reduce production to keep these costs low. As they reduce production, the market price will increase as supply is less.

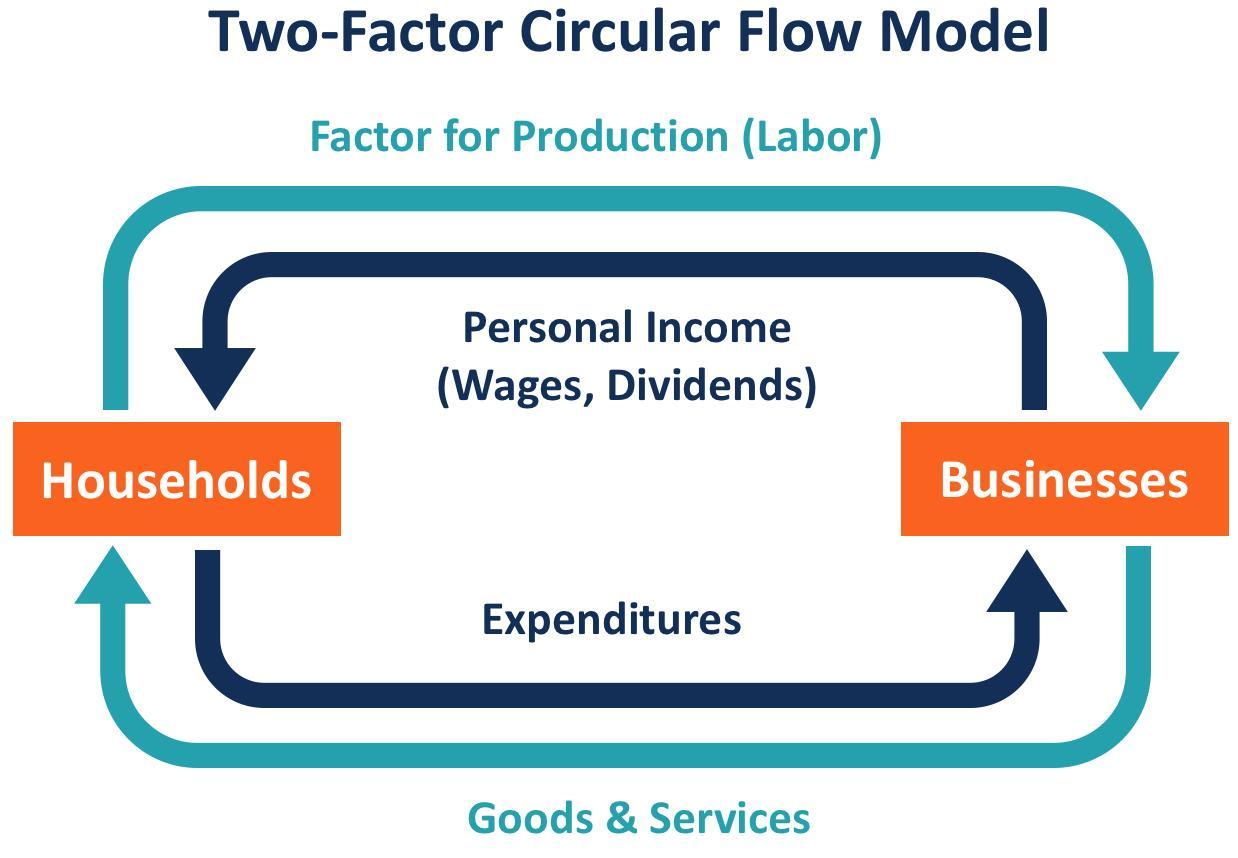

It should be noted that in the circular flow model, the resource markets provide for the exchange of labor, and product markets provide for the exchange of goods and services.

- The circular flow model simply shows how money moves in society. The three main actors in the circular flow of income are the households, firms, and the government.

- For example, in the model, the households give money to businesses after goods are bought. The government also taxes businesses. The businesses pay the people salaries, etc. It just shows how money moves in an economy.

Read related link on:

brainly.com/question/3192891