Answer:

It will be a net gain for 6,325.2 after taxes

Explanation:

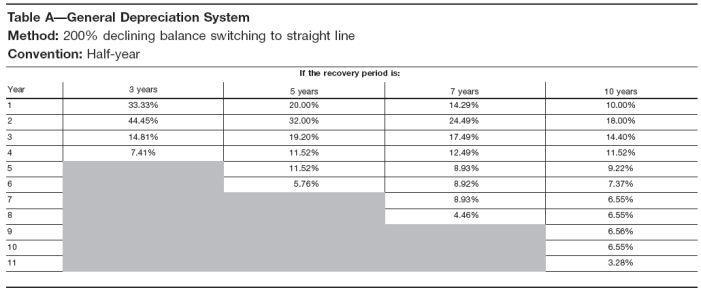

Bases on the MACRS at the end of the third year. we will have a book value of 7.41% Remember that under MACRS we have a half year convention so we depreciate for half a year on the assets first year. given a total year of useful life + 1

40,000 x 7.41% = 2.964

sales price: 12,000

we will pay taxes for the difference:

12,000 - 2,964 = 9.036

9036 x (1 - 30%) = 6.325,2

Answer:

A. Destination Contract

Explanation:

A destination contract is a contract or an agreement between the seller and the buyer of products. The contract is such that the risk of loss is stated explicitly that until the buyer takes delivery of the goods at his agreed destination, then the risk of loss is to be borne by the seller.

The agreement is based on the knowledge that it is the responsibility of the seller to get his goods to the buyer and until that is done, any risk such as loss of goods or destruction of goods are to be paid for by the seller.

A destination contract should be therefore specified by Custom Windows Inc which indicates that any form of loss or risk that might occur before the goods get to Kacey will be borne by the company.

Answer:

Machine K

Explanation:

The values can be better computed as:

Year 0 1 2 3

J 11000 1200 1`300

K 13000 1200 1300 1400

Using the PV Calculator

The Present Value (PV) for each year in Machine J is as follows:

Cashflow Year Present Value

11000 0 11000

1200 1 1085.97

1300 2 1064.68

Total 13,150.65

The effective annual cost =

= $7628.16

Using the PV Calculator

The Present Value (PV) for each year in Machine K is as follows:

Cashflow Year Present Value

13000 0 13000

1200 1 1085.97

1300 2 1064.68

1400 3 1037.63

Total 16,188.28

The effective annual cost =

= $6566.92

Therefore, machine K is better to buy than machine J.

Answer:

Option E It is multiplied by the material unit cost to calculate the per unit carrying cost.

Explanation:

The reason is that the carrying cost which is also known as holding cost is the cost of holding a unit material for a year and this can be calculated as:

Holding Cost is also given in percentage of material price and is calculate by multiplying it with the material unit cost to calculate the holding cost per unit per year.

So the option E is correct.

Answer:

What is the term used to describe product attributes that attract certain customers and can be used to form the competitive position of a firm?

Competitive dimensions.

Explanation:

In the business world, there are companies that sell products that are used for the same things. The companies in this types of environments are in competition with each other since they are all fighting over the same resource which is market share. A bigger market share usually translates to more customers and more sales. Bigger sales reflects to a bigger profit margin. For a company to have a bigger market share, there are a number of things that they can do to form the competitive position of their firm. They can do this by using product attributes that attract certain customers, a situation termed competitive dimensions.

The following competitive dimensions can be considered, namely;

1. Quality: companies can focus on the quality of their product by improving the quality of the features above the competition. In this way some customers might consider opting for that product because of its perceived quality. The major features of quality are: reliability, performance, serviceability and value for money.

2. Time: the following form the major components of time, namely; delivery time, manufacturing lead-time and frequency of delivery.

3. Price and cost: these include selling price and the service costs.