Answer:

Present value (PV) = $100,000

Number of years (n) = 12 years

Future value (FV) = $240,000

FV = PV(1 + r)n

$240,000 = $100,000(1 + r)12

<u>$240,000</u> = (1 + r)12

$100,000

2.4 = (1 + r)12

12√2.4 = 1 + r

1.0757 - 1 = r

0.0757 = r

r = 0.0757 = 7.57% = 8%

Explanation:

In this case, we need to apply the formula for future value of a lump sum (single investment). The present value, future value and number of years have been provided in the question with the exception of interest rate. Thus, interest rate becomes the subject of the formula,which implies that we will solve for interest rate.

Answer:

D) Quantity sold rose while the effect on price is ambiguous.

Explanation:

Two separate things happened here;

- Change in consumer habits have shifted the the demand curve to the right, increasing the quantity demanded at every price level.

- Better technology and lower costs have also shifted the supply curve to the right, increasing the quantity supplied at every price level.

One thing is certain, the quantity demanded and supplied increased, so the total quantity sold definitely increased. The price issue is not certain because you would need additional information about which shift was larger, the shift of the supply curve or the demand curve.

Answer:

c

Explanation:

Breakeven quantity are the number of units produced and sold at which net income is zero

If the sales of a company exceeds the breakeven quantity, the firms is earning a profit.

If the company's sales is less than the Breakeven quantity , the firm is making losses that would not be recouped

Breakeven quantity = fixed cost / price – variable cost per unit

150,000 / (5 -3) = 75000

Answer:

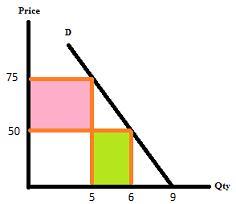

False

Explanation:

If Jake decides to increase total sales volume by decreasing the price of its engines, the decrease in price is too large compared to the increase in quantity demanded. The number of engines sold will increase from 5 to 6 (1 more unit) while the price of each engine will decrease from $75,000 to $50,000.

In this scenario, engines are price inelastic:

PED = % change in quantity demanded / % change in price = [(6 - 5) / 5] / [($50,000 - $75,000) / $75,000] = (1 / 5) / ($25,000 / $75,000) = 0.2 / 0.33 = 0.6

when PED is less than 1, the demand is inelastic. This means that a decrease in price will result in a smaller proportional increase in quantity demanded.

Explanation:

This question is imprecise, because the reason for the existence of business is to satisfy the needs of consumers, being characterized as an economic activity whose main objective is to generate profits.

Therefore, the economic needs of society are not met by companies at the expense of the suffering imposed on their customers, since the goods and services produced exist to satisfy the human needs necessary for a better quality of life.

It is also important to emphasize that, currently, there is a new interaction between company and consumer, where there is a much more direct relationship, where there is a social demand that companies be much more than just profitable entities, consumers expect companies to exercise a social role of contributing to the social and environmental development of the macroenvironment in which it is inserted. Therefore, a company that does not exercise corporate governance in the globalized world, has little conditions to remain in the market in the long run.