Answer:

Carter's preferred stock nominal annual expected rate of return is 8.12%.

Explanation:

Nominal annual expected rate of return of a preferred stock can be described as the current or unadjusted rate of return of the stock.

The nominal annual expected rate of return can be calculated as follows:

Nominal annual expected rate of return = Annual preferred stock dividend per share / Preferred stock price ............. (1)

Where;

Annual preferred stock dividend per share = Dividend per quarter * 4 = $1.40 * 4 = $5.60

Preferred stock price = $69.00

Substituting the values into equation (1), we have:

Nominal annual expected rate of return = $5.60 / $69.00 = 0.0812, or 8.12%

Therefore, Carter's preferred stock nominal annual expected rate of return is 8.12%.

Answer:

Try try but don't cry I think we don't lose our hopes

Answer:

E. They will receive several tax deductions

Explanation:

Certain "reasonable and necessary" adoption related expenses are quantifiable for tax deductions, such as:

- Court costs

- Attorney's fees

- Traveling expenses related to the adoption

- Certain other costs directly related to the adoption process

Answer:

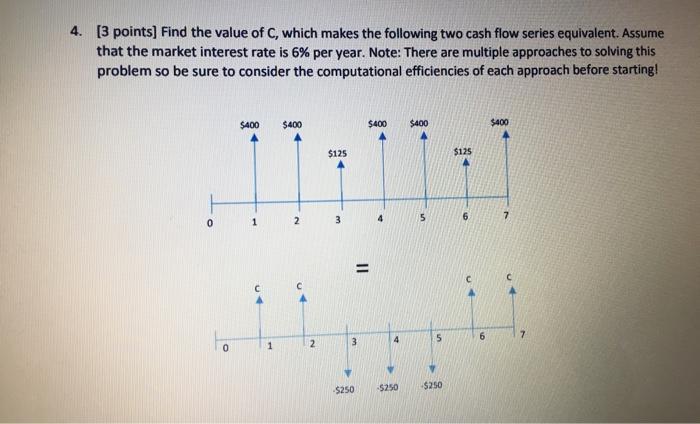

Find attached complete question.

$ 750.10

Explanation:

In order to ascertain the value of C ,we need to equate the present value of the two streams of cash flows to each other as follows:

first stream:

$400/(1+6%)^1+$400/(1+6%)^2+$125/(1+6%)^3+$400/(1+6%)^4+$400/(1+6%)^5+$125/(1+6%)^6+$400/(1+6%)^7=$1,808.19

Second stream:

C/(1+6%)^1+C/(1+6%)^2-$250/(1+6%)^3-$250/(1+6%)^4-$250/(1+6%)^5+C/(1+6%)^6+C/(1+6%)^7

-$250/(1+6%)^3-$250/(1+6%)^4-$250/(1+6%)^5=-$594.74

C/(1+6%)^1+C/(1+6%)^2+C/(1+6%)^6+C/(1+6%)^7=C/0.9434+C/0.8900+C/ 0.7050+C/ 0.6651

simplification

C/0.9434+C/0.8900+C/ 0.7050+C/ 0.6651=C/(0.9434+0.8900+0.7050+0.6651)= 0.31216C

All in all:

$1,808.19 =-$594.74+ 0.31216C

$1,808.19+$594.74= 0.31216C

$2402.93

= 0.31216C

C=$2402.93* 0.31216 =$ 750.10

Answer:

Part 1.

The negotiable range for the transfer price is between is $6 to $18 as the Netting division will incur loss if it sells its product below its variable cost whereas the maximum price it can transfer the product to Basketball equipment department is equal to the selling price that is $18.

Therefore, negotiable range is between for the transfer price is $6 to $18.

Part 2.

The minimum transfer price the Netting division should consider if at operating capacity is $18.

If they are at below capacity, the minimum transfer price would be $6.

Part 3.

The maximum transfer price the basketball equipment division should consider must be equal to the price outside vendors are charging for the same quality product that is $15.

Therefore, the maximum transfer price the Basketball Equipment Division should consider is $15.