Answer:

Standard cost = $5.57

Explanation:

As per the data given in the question,

Standard cost = Standard usage * standard price

Ingredient Amount/gallon st. waste St. usage St. price St. cost

Lime 24.0 Oz 4% .96X=24.0 Oz=25 Oz 0.15 $3.75 kool-drink

Sugar .72 lb 10% .90X=.72 lb = 0.8 lb $0.65 $0.52

Protein tablets 2 0% 2 $0.40 $0.80

Water 50 Oz 0% 50 Oz $0.01 $0.50

Total $5.57

Total standard cost = $3.75 + $0.52 + $0.80 + $0.50

= $5.57

All incoming mail except original court documents

Answer:

I have just received seed money for a new e-commerce business and you want to hire a dozen people with a lot of creative potential. To hire the most creative people, you would select applicants who:

Has above-average intelligence, is persistent, has subject-matter expertise, and an inventive thinking style.

Explanation:

Starting a new e-commerce business required the need for hire experienced personnel with creative thinking style in order to spur the business to the peak inline with vision and mission set for such businesses

Answer:

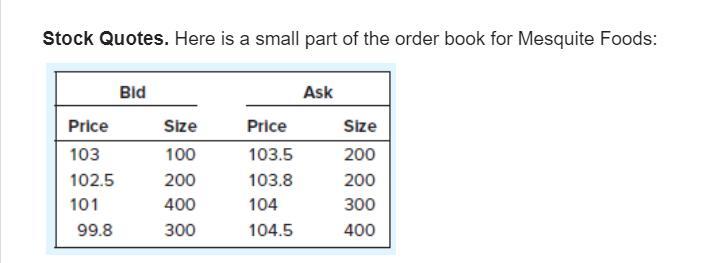

The question is missing stock quotes which are found in the attached.

The maximum price that Norman Pilbarra will pay to buy 400 shares is $103.8 per share.

Explanation:

Judging from the attached stock quotes,the first 200 shares offered for sale is $103.5 per share while the next 200 shares is at a price of $103.8.

This then means that the maximum price for 200 shares is $103.8.This information is derived from the ask prices not bid prices since ask price is for sale,whereas bid is for purchase.

Answer:

A.

Dr merchandise inventory 47,040

Cr Account payable 47,040

B.

Dr Account payable 7,350

Cr merchandise inventory 7,350

C.

Dr Account payable 39,690

Cr Cash 39,690

D.

Dr Account payable 39,690

Dr Purchase discount 810

Cr cash 40,500

Explanation:

Stylon Co. Journal entry

A.

Dr merchandise inventory 47,040

Cr Account payable 47,040

(48,000-(48,000×2%)

B.

Dr Account payable 7,350

Cr merchandise inventory 7,350

(7500-(7500×2%)

C.

Dr Account payable 39,690

Cr Cash 39,690

(47,040-7,350)

D.

Dr Account payable 39,690

Dr Purchase discount 810

(48000-7500)×2%

Cr cash 40,500