Answer:

True.

Explanation:

It is a true statement.

The firm economic result that is, financial performance depends upon various factors that includes external forces also.

Further, to remain in industry ( or for stable growth ), the firm have to synchronize their activities with the environment.

The question specifies economic environment that relatively impact the firm. So , this statement is true.

Answer: 1. A . Treasury bonds are not completely riskless, since their prices will decline when interest rates rise.

2. A. The New York City government

3. B. Municipal bonds

4. A. An investor from Kansas that invests in a municipal bond issued by the State of Kansas will pay neither state nor federal taxes on the bond’s coupon payments

5. B. Treasury bonds

Explanation:

1. Treasury Bonds are known as the safest bonds in the world and so are generally considered risk-less. However this is not so as they still fall victim to Interest rate risk which is the risk that their prices will decline when interest rates rise because bond prices are inversely related to price.

2. The City of New York issued to bonds in question so it is a New York City Government bond.

3. Municipal Bonds are issued by a state, county or a municipality so the above is a Municipal bond as it was issued by the City of New York.

4. Municipal Bonds attract no Federal taxes and when buying a Municipal bond as a resident of the Municipality you are in, you will.not get charged the Municipal taxes either on the bond coupon payments.

5. Default risk is the risk that the issuer will not pay back. US Treasury Bonds are known as the safest in the world and have not been defaulted on in over a century. They therefore have the lowest default risk.

Answer:

required rate of return on the stock = 22.7%

so correct option is e. 22.7 percent

Explanation:

given data

risk free rate = 4 percent

rate of return = 15 percent

beta = 1.7

to find out

required rate of return on the stock

solution

we get here required rate of return on the stock that is express here as

required rate of return on the stock = risk free rate + beta × ( Return on the Market portfolio - Risk free Rate) ........................1

put here value we get

required rate of return on the stock = 4 + 1.7 × ( 15 - 4)

required rate of return on the stock = 22.7%

so correct option is e. 22.7 percent

B, it's a steady mortgage rate that won't change.

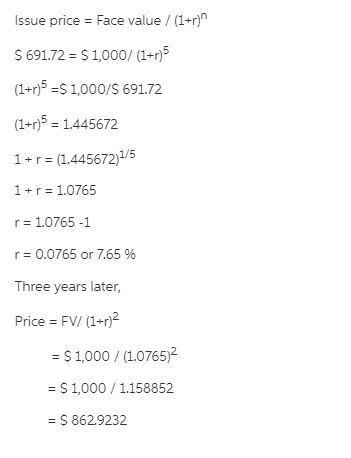

Answer:

Following is given the solution for given question.

I hope it will help you a lot!

Explanation: