Do you have a question about it?

Answer:

Explanation:

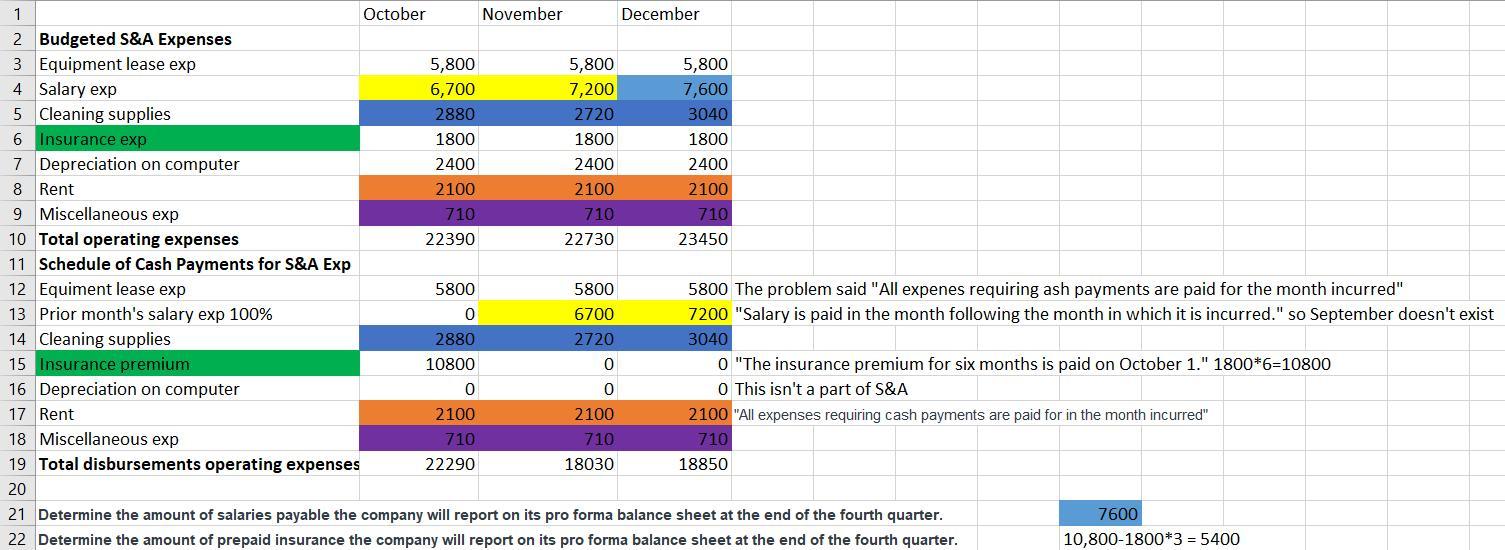

c. Determine the amount of prepaid insurance the company will report on its pro forma balance sheet at the end of the fourth quarter.

The answer is 5400 because "at the end of the 4th quarter is only consists of 3 months (oct-dec). By taking the total amount you paid for all 6 months minus what you have to pay for 3 months.

Answer:

$5,500 USD

Explanation:

Since traditional Roth IRA accounts cannot be owned jointly, then both individuals must have their own account. That being said they can still contribute to each other's Roth IRA accounts on behalf of their spouse. You can contribute a total of 100% of your earned income up to a limit of $5,500 USD. Pensions are not allowed as contributions. Individual's over the age of 50 have a limit of $6,500

Answer:

No, contracts for personal services are not assignable.

Explanation:

According to a different source, these are the options that come with this question:

Yes, as long as the assignment does not increases the burden on Max.

Yes, Claire can assign her obligations under the contract to anyone who accepts.

No, contracts for personal services are not assignable.

No, the assignment is not valid since Max did not give any consideration.

This is most likely not a good strategy for this woman. The fact that this woman has been hired as a freelance web designer means thta the woman is beig paid for her professional expertise. No one else can perform the job in the way that she can perform it. Therefore, she cannot assign this duty to another person.