Answer:

$557,000

Explanation:

Note: <em>Missing word is attached as picture below</em>

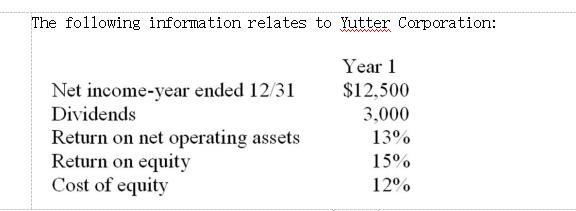

Retention Ratio = (Net Income - Dividends) / Net Income

Retention Ratio = (12500 - 3000) / 12500

Retention Ratio = 9500 / 12500

Retention Ratio = 0.76

Retention Ratio = 76%

Sustainable equity growth rate = Retention Ratio * Return on Equity

Sustainable equity growth rate = 76% * 15%

Sustainable equity growth rate = 11.40%

Expected dividend per share = Current Year Dividend *(100 + Growth Rate)%

Expected dividend per share = 3000 * (100+11.4)%

Expected dividend per share = 3000 * 111.4%

Expected dividend per share = 3342

Value of Stock = Expected dividend per share / (Cost of capital equity - Dividend growth rate)

Value of Stock = 3342 / (12% - 11.40%)

Value of Stock = $557,000