Answer:

At face value

Explanation:

Short term notes are always recorded at face value, and that applies to both interest and non-interest bearing short term notes.

Non-interest bearing long term notes must be recorded at their discounted value, i.e. you must discount the long term note' face value by the discount rate used by the company.

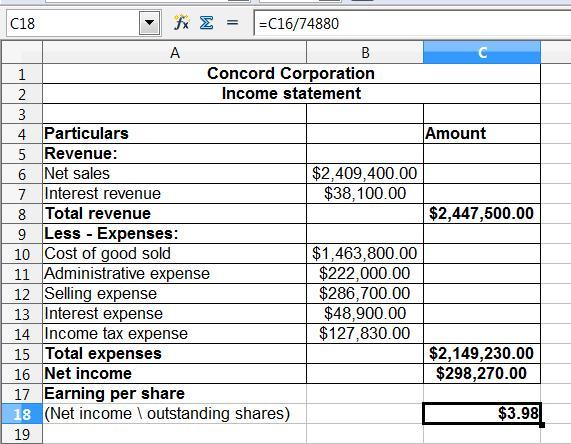

Answer:

Explanation:

In the income statement, the total revenues and the total expenses are recorded.

If the total revenues are more than the total expenditure then the company earns net income

And, If the total revenues are less than the total expenditure then the company have a net loss

This net income or net loss would reflect in the statement of the retained earning account.

The calculation is shown below:

= Net Sales + interest revenue- cost of good sold - administrative expense - selling expenses - interest expense - income tax expense

where,

Income tax expense = (Net Sales + interest revenue- cost of good sold - administrative expense - selling expenses - interest expense) × income tax rate

= ($2,409,400 + $38,100 - $1,463,800 - $222,000 - $286,700 - $48,900) × 30%

= $426,100 × 30%

= $127,830

The preparation of the income statement is presented in the spreadsheet. Kindly find the attachment below:

Answer:

Pauls' share in partnership=(131000+91000+111000+171000)*0.15%= $75600

Balance in Caitlin’s capital account immediately after Paul’s admission = 131000-(75600-71000)*30%= $129160

Answer:

November 6th is the last date to exercise the rights.

Explanation:

The shareholders have right to sell the rights to other shareholder, for which the shareholders need to exercise the rights before the right issue. If the shareholders doesn't makes any exercise of right issue before date then he is not entitled to rights anymore. The last date is the date on which the payment is made.