Health hazards are hazards that are health related, not safety hazard! Loose railings, hot water, and blocked doorways are safety hazards, but they aren't bad for your health. Moldy floorboards could be hazardous towards your health, so that's your answer!

Answer:

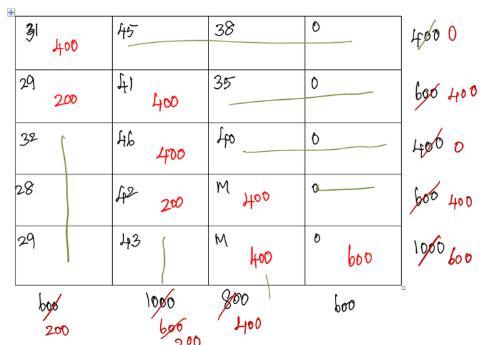

A parameter table was constructed to show the transportation problem and to also obtain an optimal solution.

Explanation:

<u>Solution</u>

(a) the first step is to prepare the problem as a transportation problem by establishing the appropriate parameter table

1 2 3 Supply

Source 1 31 45 38 400

(Plant) 2 29 41 45 600

3 32 46 40 400

4 28 42 M 600

5 29 43 M 1000

Demand 600 1000 800

The total supply is = 400 + 600 + 400+ 600+ 1000= 3000

Total demand is = 600 + 1000 + 800 = 2400

(b) since the problem given is an imbalanced transportation problem,to make it a balance transportation problem we will make use of what is called the dummy destination for this numbers 3000 - 2400 = 600

1 2 3 4 (Dummy) Supply

Source 1 31 45 38 0 400

(Plant) 2 29 41 45 0 600

3 32 46 40 0 400

4 28 42 M 0 600

5 29 43 M 0 100

Demand 600 1000 800 600

The positive independent number of allocations is equal to m+n -1 = 5 + 4-1 =8

This solution is a basic feasible solution called a non -degenerate

The cost of initial transportation is he initial transportation cost=31*400+29*200+41*400+46*400+42*200+M*400+M*400+0*600

=$61400+800M

Note: kindly find an attached document of the part of the solution of the work.

Answer:

depends on how much you already have...

Explanation:

First off you need to know what they mean. Trend means what people are in to and want to buy. Supply is how much the sellers have of items. If you have a huge supply of something that isn't in trend then you won't have any business. If you have a huge supply of something that is in trend, people will buy a lot of it. It is a factor of business like supply and demand. I hope this helped :)