Answer:

A. a separate schedule.

Explanation:

This is explained to be cash flow schedule or also cash flow statement. It is explained to be on out of the three financial statement which used generally to report for cash which been generated and how this money has been totally been spent within a period or interval which could be a week, month, quarter or even probably a year.

In the statement of cash flows, the cash flows are known to be generated from investing activities section while inclusion of receipts from the sale of investments. This is why in the stated 20 year payable bond, it is known to have been recorded in statement of cash flows in a separate schedule.

Answer:

Check the following explanation.

Explanation:

Corporation has no accumulated E & P at the time of the distribution. The shareholder has a taxable dividend equal to the current E & P determined at year-end, which was $40,000. The balance of the distribution,$20,000, reduces the shareholder’s basis in the stock, and any excess over basis results in capital gain.

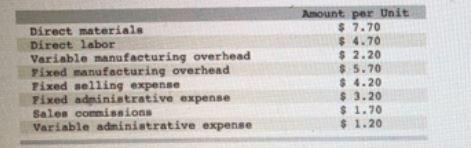

Based on the details given, the following are true:

- 1. Incremental manufacturing cost = $14.60

- 2. Incremental cost = $17.50

<h3>Incremental manufacturing cost if production increased from 20,250 to 20,251</h3>

The fixed cost will not change as the production amount is still below 24,500 units. Incremental manufacturing cost will therefore be:

= Direct material + Direct labor + Variable overhead

= 7.70 + 4.70 + 2.20

= $14.60

<h3>Incremental cost for increased from 20,250 to 20,251</h3>

This will include all costs that are not fixed.

= Incremental manufacturing cost + Sales commissions + Variable admin expense

= 14.60 + 1.70 + 1.20

= $17.50

Find out more on incremental manufacturing cost at brainly.com/question/8527680.

What are you asking in this question I’m just confused, could you write it in the comments

Answer: Option A

Explanation: Outsourcing can be defined as a situation in which a company hires another company for performing some activities that are non core for the hiring companies.

For, example a company having business of making soft drink might outsource its advertising activity.

One problem with outsourcing is that it leads to no internal control of the hiring company's management on that particular activity, leading to high probability of fraud or failure.

Thus, if an activity needs internal control it should not be outsourced.