Answer:

$0.69 million or $690,000

Explanation:

Value of Firm Vₐ = $24.7 million

Debt D = $5.5 million

Shares S = 390,000 * 51 = $19.89 million

Therefore Value Vₓ = 5.5 + 19.89 = $25.39 million

We would expect Vₐ and Vₓ to be the same value. Therefore the decrease in the value of the company due to expected bankruptcy costs is

= $25.39 million - $24.7 million

= $0.69 million

Answer:

$125,165.49

Explanation:

Daily Sales Outstanding is computed by dividing Average Accounts Receivable over Daily Credit Sales.

In this case, if the DSO is 71, then the Daily Credit Sale is $2,887.3239($205,000/71).

Then, the old sales is $1,053,873.24 ($2887.3239 x 365).

If this is reduced by 15% after the policy is implemented, the new sales is $895,792.25 ($1,053,873.23-15%) and the new daily sales is $2,454.23 ($895,792.25/365).

Using these DSO formula, the new Accounts Receivable level will be $125,165.49 (51 x $2,454.23).

Answer:

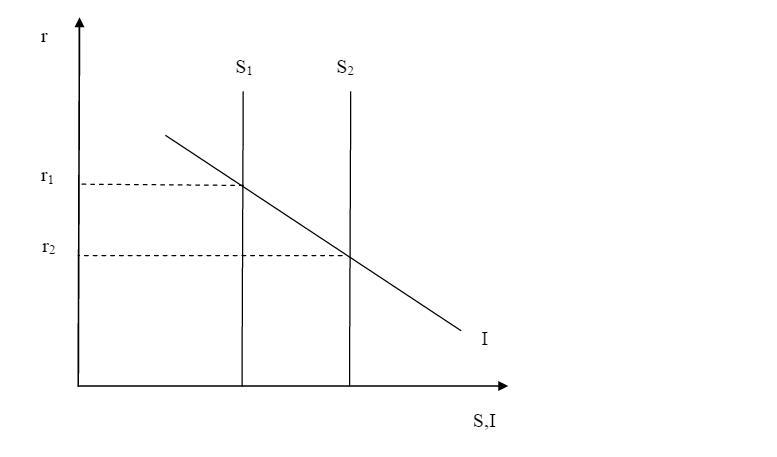

real interest rate decreases, national saving increases, investment increases, consumtion is unchhanged, output is unchanged (fixed because it is determined by the factors of production).

Explanation:

Answer:

OPTION C = 51%

Explanation:

<em>Percentage of federal tax revenue which comes out of individuals paycheck</em>

<em>=individual income tax+corporate income tax</em>

given that,

individual income tax=42%

corporate income tax=9%

Hence, Percentage of federal tax revenue which comes out of individuals paycheck

=42%+9%

=51%

Answer:

Manufacturing cost= $92.5

Explanation:

Giving the following information:

Predetermined overhead rate= $4.2 per machine hour

Job 664:

2.5 machine hours

$26.00 of direct materials

4 hours of direct labor for $14 per hour.

<u>To allocate overhead, we need to use the following formula:</u>

Allocated MOH= Estimated manufacturing overhead rate* Actual amount of allocation base

Allocated MOH= 4.2*2.5= $10.5

<u>Now, the manufacturing cost:</u>

Manufacturing cost= 10.5 + 26 + 4*14

Manufacturing cost= $92.5