Answer:

To ensure assets and liabilities are reported at appropriate amounts.

To ensure the related revenues and expenses are reported in the proper period.

Explanation:

Adjusting entries at the end of the period are basically made, to comply with the requirements of the accrual principal.

Under accrual principal the financial statements represent the true and fair view of the transactions and conditions of the company.

It basically records all the revenues and expenses at the time when they are incurred and not at the time when they are paid in cash, or cash is received.

As and when the transaction incurs, or to the period it relates it shall be disclosed.

Therefore, each balance sheet item is disclosed and reported at the appropriate amount. And the all the revenues and expenses related to the period are provided for.

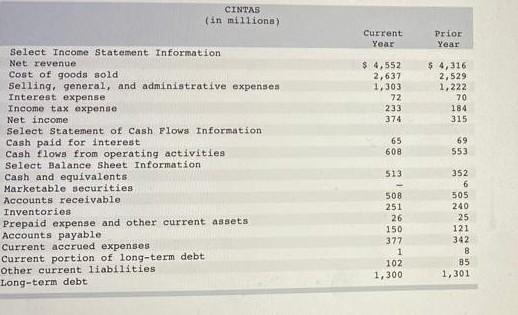

According to tha data,

Receivable stock Turnover ratio = Credit sales / Average debtor

= $4,552 / ($505+$508)÷2

= $4,552 / $506.5

= 8.99

Inventory stock Turnover ratio = Cost ot goods sold / Average Inventory

= $2,637 / ($251+$240)÷2

= $2,637 / $245.5

= 10.74

Current ratio = Current assets / current liabilities

Current assets=$513+$508+$251+$26 = $1,298

Current Liabilities = $150+$377+$1+$102 =$630

Current ratio = $1,298 / $630

= 2.06

Cash ratio = Cash and cash equivalents / Total current liabilities

= $513 / $630

=0.81

Tines Interest earned ratio = Earnings before interest and tax (EBIT)/ Interest

EBIT = Net income + Tax expense + Interest expenses

= $374 + $233 +$72

= $679

Times interest earned ratio = $679 / $72

= 9.43

Cash Coverage ratio = Cash flows from operating activities / Cash paid for interest

= $608 / $65

= 9.35

Learn more about stock here:

brainly.com/question/25818989

#SPJ4

Answer:

b) A decrease in ownership percentage from 25% to 15%

Explanation:

There is change in accounting method when the shareholding is 20% or more.

Under Consolidation there are two methods:

Equity method: This is used when the shareholding is 20% or more, and there is significant influence. Under this method all the assets and liabilities are accumulated in the consolidated balance sheet.

Proportional Consolidation method: This is generally used when the shareholding is merely shown as an investment, and the balances of assets and liabilities are not accumulated.

Thus, there is a change in method of accounting when the shareholding is more than 20%. This is in case b as change is from 25% to 15% and thus, it will change from equity method to proportional consolidation method.

Answer: Vroom and Yetton's normative decision model.

Explanation:

The Vroom–Yetton normative decision model is a situational leadership theory of industrial and organizational psychology that was developed by Victor Vroom, in collaboration with Phillip Yetton and later with Arthur Jago. The situational theory argues the best style of leadership is contingent to the situation.

Regarding decision making, the Vroom-Yetton model suggests that being autocratic, seeking advice, considering alternative approaches before a decision is made, informing a group on an issue, and letting that group develop the solution without forcing your own ideas are all important at times.

Answer:

C) used to record an adjustment to Bad Debt Expense for the year ending December 31, 2021.

Explanation:

Retained earnings account cannot be adjusted after December 31 (or whenever the balance must be done), but bad debt expense can be adjusted, specially if it increases.

Generally a company estimates it bad debt expense, the different methods used to estimate bad debts (allowance, percentage or aging methods) are used more commonly than the direct write-off method. But as every estimate, they can be close to reality or not.

E.g. some companies might have a very important client that represents a large portion of their credit sales, and if suddenly that large client that had always paid on time defaults, that event must be included in the balance sheet since the bad debts expense will increase significantly.