Heyyyyyy thanks for the points, have a nice day/night wtv :)

Answer:

Tractors are the king among different farm equipment. They are the main workhorse of any modern farm. They provide the power and traction necessary to mechanize agricultural tasks. ... There are different types of tractors in the market, varying in size and capacity.

Explanation:

Answer:

At the end of one accounting period result in cash receipts in a future period.

Explanation:

Accrued revenues is money owed by customers for goods bought or services purchased.

Accrued revenue is recorded as an asset on the balance sheet as receivables.

For example, if a customer buys a dress and is yet to pay for the dress. the amount the customer is supposed to pay is recorded as an accrued revenue at the end of the accounting period

Unearned revenue is money received by a company for services that are yet to be rendered.

Answer:

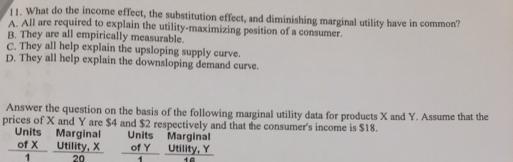

They all help explain the downsloping demand curve

Explanation:

The options to the question wasn't provided. The complete question can be in the attached image.

The demand curve slopes downward from left to right. This indicates that the higher the price, the lower the quantity demanded and the lower the price, the higher the quantity demanded.

Income effect is a change in quantity demanded when real income change. Quantity demanded increases when real income increases and decreases when real income falls.

Substitution effect says that consumers would substituite to the consumption of a cheaper good when the price of a good originally consumed increases.

Diminishing marginal utility states that as consumption increases, utility derived from consumption falls and quantity demanded falls.

I hope my answer helps you

Answer:

Extinction

Explanation:

Contingency of extinction occurs when previously reinforced behaviours are removed or changed as a result of changes in the environment. In this scenario, the behaviours that was changed in the current year was the payments of bonuses to top managers. The changes in the environment was the poor performance and average stock price dropping. It resulted in the top managers not receiving their annual bonuses this time.