<span>GDP = C + I + G + NX = $5.5 trillion + $1 trillion + $1.5 trillion + $.75 trillion - $1.25 trillion = $7.5 trillion

Business is hard T^T</span>

I believe the answer is D.

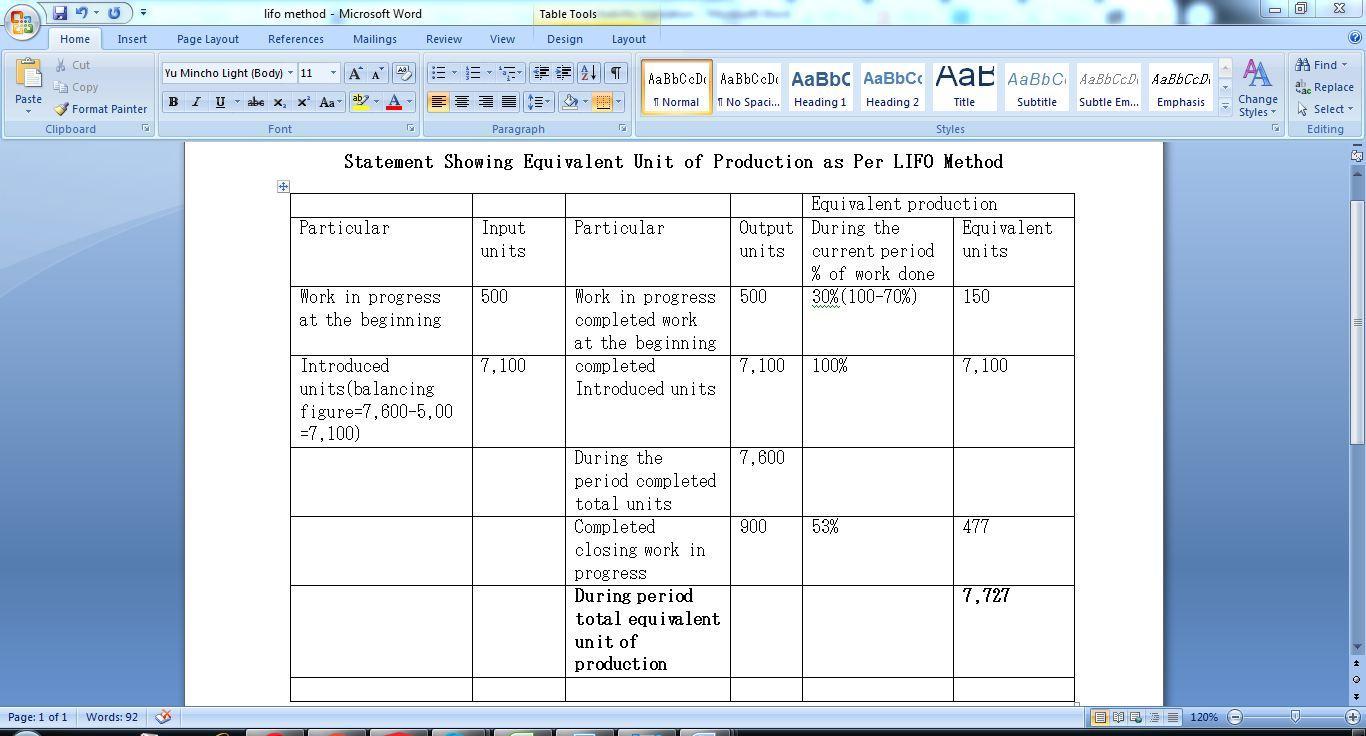

Answer:

7,727 units

Explanation:

According to the scenario, computation of the given data are as follows:

Department S beginning = 500 units

Completed % in process = 70%

Total completed during period = 7,600 units

End of period = 900 units 53 % completed

So, we can calculate the units of production using FIFO method.

Check attachment for the Solution.

The attachment is attached below.

Answer: Stakeholder

Explanation:

The stakeholder is the person in an organization that manage all the external and the internal function or the stake of the business.

The main objective of the stakeholder is to managing all the resources, stake, knowledge and the materiel of the company and it also provide some interest to an organization.

According to the question, the stakeholder is basically supply the various types of productive resources ti the firms and then claim on the stake in an organization and this is known as stakeholder.

Therefore, Stakeholder is the correct answer.