Answer:

The correct answer is letter "A": One thing I am afraid to say in this group is...

Explanation:

Managers portraying weak images typically end losing control over their subordinates affecting a company's efficiency and effectiveness. Leaders must always be willing to impose their ideas when convenient for the whole group. They must provide firm, strong orders under those situations for the common benefit of their team. Mentioning employees:

"<em>One thing I am afraid to say in this group is...</em>";

shows the manager is not even sure of what he thinks. It is important to take into consideration the subordinates' points of view but before that, the leader must be sure of what he or she is doing.

The gross domestic product (GDP) of the United states is defined as all the final goods and services produced in a given period of time.

<h3>What is Th

e gross domestic product of a country?</h3>

The gross domestic product of a country is all the final goods and services produced in a given period which is usually a year.

One of the methods used to calculate GDP is the expenditure method and it entails adding together the following components: consumption spending by households, Investment spending by businesses , Government spending and Net export

To learn more about GDP, please check: brainly.com/question/15225458

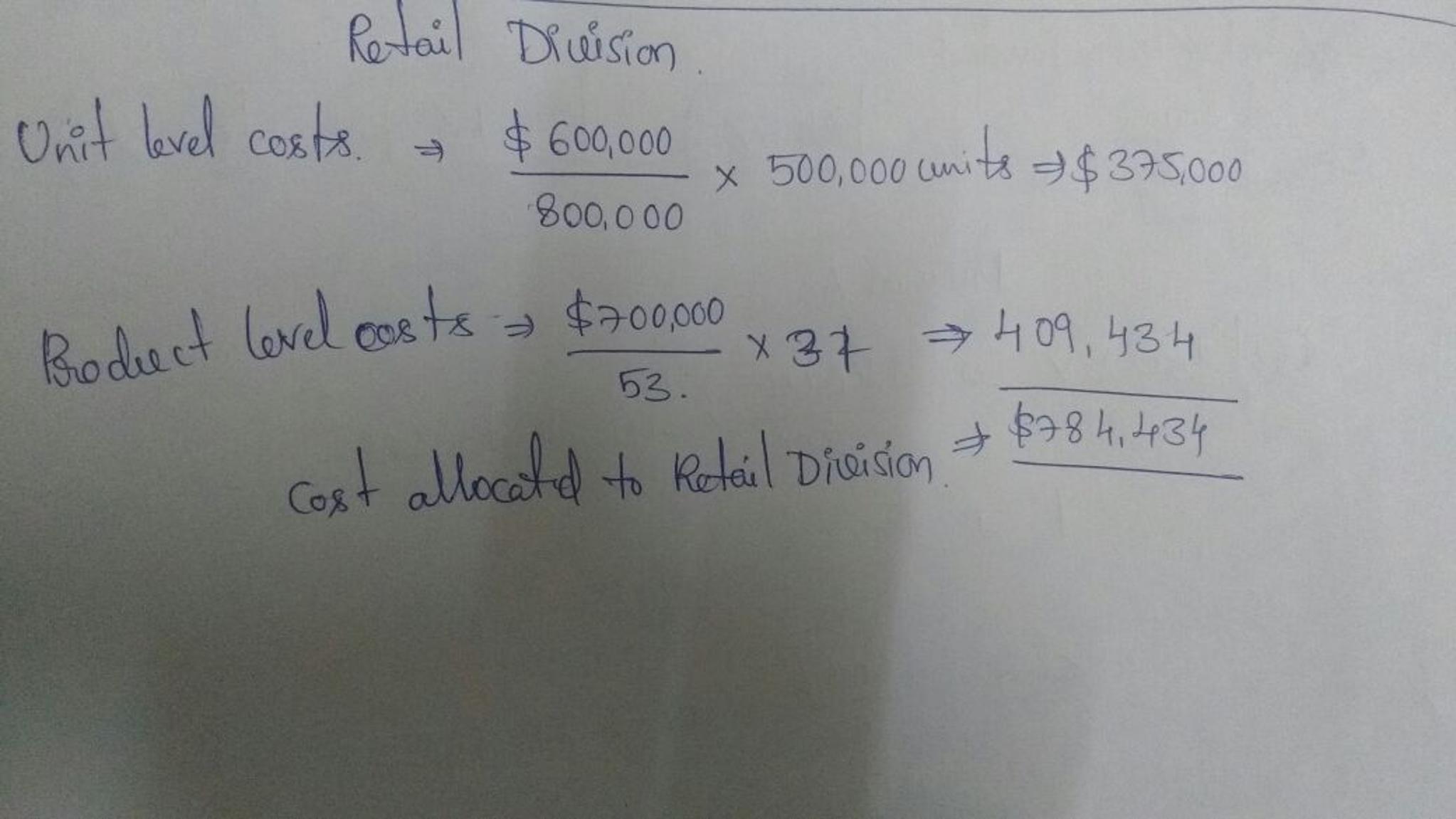

Answer:

$784,434 will be allocated to the Retail division

Explanation:

See attached file

Answer:

A general rule of thumb among marketing researchers is to use secondary data first and then collect primary data.

hope it helps:)

mark brainliest!