Answer:

a. $418,000

Explanation:

The computation of the contribution margin of the West business segment is shown below:

Contribution margin = Sales revenue - variable expenses

= $890,000 - $472,000

= $418,000

By deducting the variable expenses from the sales revenue we can get the contribution margin and we applied the same that is shown above.

Answer:

B

Explanation:

the knowledge.. between a Bachelor degree and an associate degree. is leser

Answer:

The Given Statement is True

Explanation:

It is true that globalization causes the businesses, countries and people to become increasingly interdependent. Globalization means operating internationally which causes the people, businesses and the countries to depend on each other. Globalization is also used to describe the increasing interdependence of countries, people and businesses.

Explanation:

Since it is given that

Acquiring value of an vacant lot = $115,000

Sale value of the vacant lot in cash = $298,000

Since the sale value is more than the acquiring value which reflects the increment in the asset for $183,000 due to which the profit is also increased for $183,000 i.e retained earnings

Now the effect is shown below:

1. Assets = Increase = $183,000

2. Liabilities = No change = $0

3. Stockholder equity = Increased = $183,000

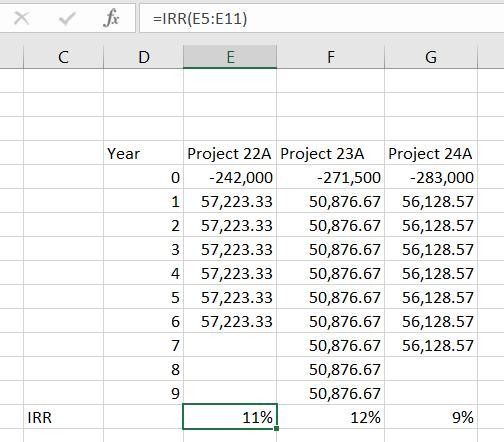

Answer:

Depreciation amount has to be added back to the annual income because it is a non cash expense.

Project 22A

Depreciation = 242,000 / 6 years

= $40,333.33

Annual income = 40,333.33 + 16,890

= $57,223.33

IRR using Excel is:

= 11%

Project 23A

Annual income = 20,710 + 271,500 / 9 years

= $50,876.67

IRR = 12%

Project 24A

Annual income = 15,700 + 283,000 / 7 years

= $56,128.57

IRR = 9%

<em></em>

<em>Note: Look at the formula bar to see how IRR was calculated. </em>