Answer:

The correct answer is all of the above

Explanation:

Scrap or the rework costs are the costs which is incurred in order to repair the items that are defective. And the decision to rework or scrap an item or product, ground on the benefits or advantage of the incremental costs.

If the reworked units generate or yield greater advantage or benefit rather than the selling them as scrap, then the decision to rework will be considered.

And if the decision of rework is taken, then the management should consider the incremental costs, revenue or profit from selling the defective units as scarp and the lost profit on selling and making the new units while the rework is performed.

Answer:

Dear Student,

I trust that this meets you well.

The question requires additional details for it to be answered.

Kindly provide the same as soon as you can.

Cheers

Answer:

Tragedy of the Commons

Explanation:

The tragedy of the commons refers to a situation where the individual could access to the resources that are shared for their own interest.

So it is the market situation where the participant expolited the resources also there is no limited for accessing the resources

So the above term should be considered for the given situation

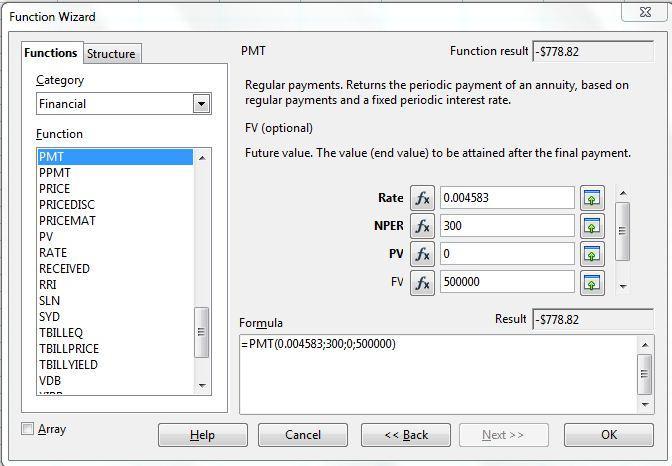

Answer:

$778.82

Explanation:

Given:

Amount to be accumulated in retirement fund which is future value (FV) = $500,000

Interest rate (Rate) = 5.5% annually or 5.5 / 12 = 0.4583%

Time period (nper) = 25 years or 25×12 = 300 periods

Monthly deposit need to be computed (PMT). which can be calculated using spreadsheet function =pmt(rate,nper,PV,FV)

=pmt(0.004583,300,0,500000)

Monthly payment is computed as $778.82

Note: PMT is negative as it is a cash outflow.

Answer:

The correct answer is letter "C": risk-free rate.

Explanation:

The United States government issues a variety of debt obligations to finance its operations. Those with the shortest maturity are called Treasury Bills or T-Bills. One of the unique features of T-Bills is that the government does not make regular interest payments to the holder. Instead, the securities are sold at a price below its face value resulting in a profit at the maturity date.

T-Bills are seen as low-risk investments compared to other securities being <em>the closest to risk-free return</em> in the market.