Answer:

reduction in investment, savings and interest rate

Explanation:

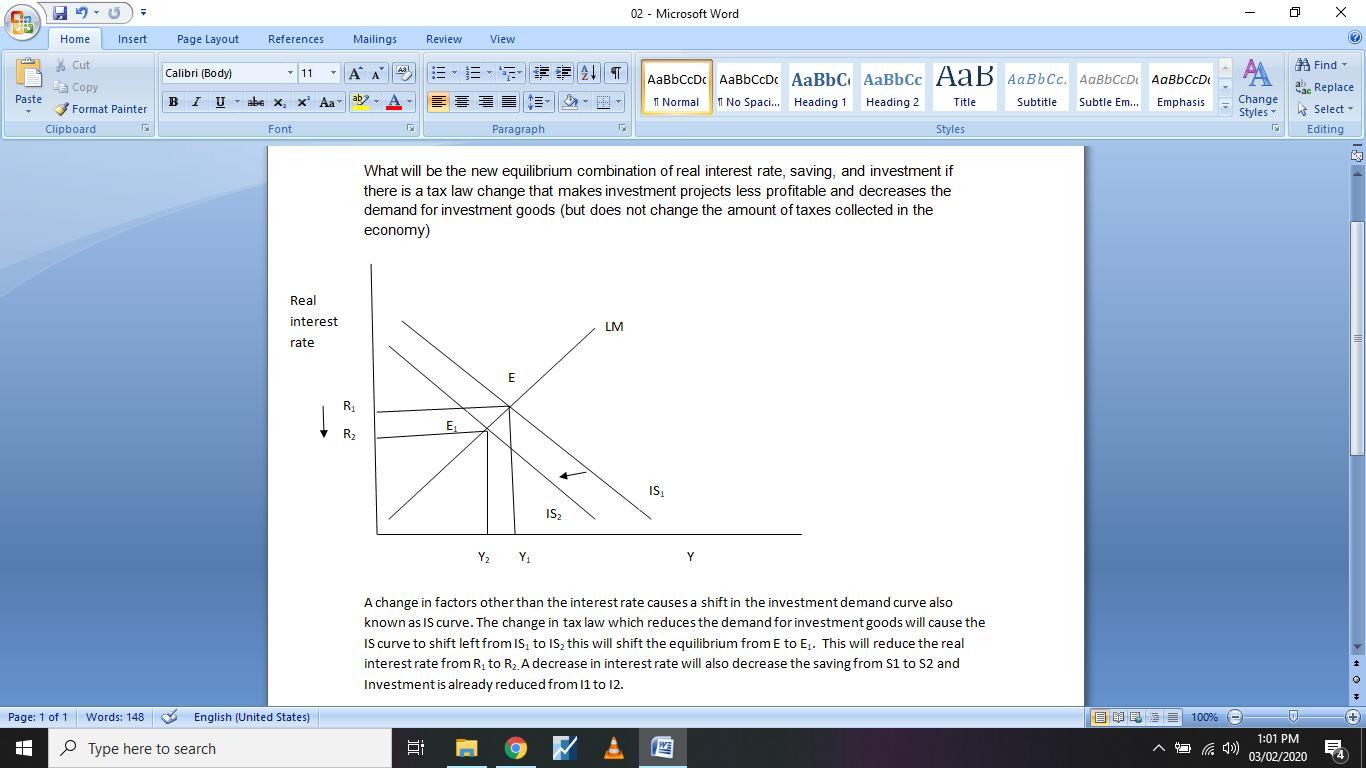

A change in factors other than the interest rate causes a shift in the investment demand curve also known as IS curve. The change in tax law which reduces the demand for investment goods will cause the IS curve to shift left from IS1 to IS2 this will shift the equilibrium from E to E1. This will reduce the real interest rate from R1 to R2. A decrease in interest rate will also decrease the saving from S1 to S2 and Investment is already reduced from I1 to I2.

Note: Graph file is attached

Answer:

The attached shows the journal entries in respect of Novark Corp. transactions for the month of October.

Every transaction has two impacts-debit and credit

Explanation:

Journal is a book of prime entry where transactions that cannot be posted to other books of original entry are treated.

Journal entry also observes the duality concept of accounting where each transaction in two accounts,for every debit,there is corresponding credit and vice versa.

Journal can also be used to correct errors made while posting to books of account.

Answer:

General purpose Job boards

Explanation:

A job board can be straightforwardly defines as a website where employers advertise job openings for job seekers

A general purpose job board as seen in the question can be defined as a website that offers job recruitment services in its entirety.

This means that both employees and employers use the site to search for and advertise job openings to job seekers respectively. Popular job boards include Glassdoor, Linkedin, etc.

Cheers.

Answer:The up-to-date ending cash balance on October 31 is: $8,290---C

Explanation:

A bank Reconciliation statement helps to match a company's book record to its bank record and adjust discrepancies, If any.

Here, the deposits in transit and outstanding checks fall under the bank's accounting records and will not be involved in the company's additions or deductions in the accounting book balance records.

Ending cash balance as per books = $7,000

Add:

Interest received from Bank = +$1,700

subtotal $8,700

Deduct

Bank Service charge = -$60

NSF check = -$350

Up-to-date ending cash balance = $8,290

Extra financial rewards, are examples of bonuses or incentives in an organization